.webp)

.svg)

Internal Controls in Accounting: Types, Examples, Guide

.avif)

Blog Summary

- What internal controls are: Policies, procedures, and system-based checks that reduce errors, deter fraud, and improve financial reporting reliability.

- What they’re for: Protect assets, support accurate and compliant reporting, and keep operations efficient.

- What you’ll get in this guide: The COSO framework, types of controls, accounting-specific examples, a step-by-step rollout plan, and an internal controls checklist accounting teams can copy and use.

What Are Internal Controls in Accounting?

Internal controls in accounting are the processes, policies, and control activities an organization uses to provide reasonable assurance that transactions are authorized, recorded accurately, assets are safeguarded, and financial reporting is reliable and compliant.

In plain English, internal accounting controls act like guardrails. They make it harder to do the wrong thing. They make it easier to catch issues early.

Reasonable assurance matters. No internal control system in accounting prevents every mistake. People override controls. Systems fail. Workload spikes. Controls reduce risk to an acceptable level.

Internal controls vs. accounting processes:

- The process records the transaction. For example, “enter the bill.”

- The control checks the process. For example, “approve the bill,” “match to PO,” or “review the vendor change.”

Internal accounting controls vs. operational controls:

- Accounting internal controls focus on financial reporting and asset protection.

- Operational controls focus on efficiency and performance.

- They overlap often. For example, better approvals reduce spend and reduce misstatements.

What Is an Internal Control System in Accounting?

An internal control system in accounting includes people, process, technology, documentation, and monitoring. Controls fail when they live in someone’s head.

When controls depend on memory, teams see patterns like these:

- Reviews happen “when there’s time.”

- Reconciliations slide past the deadline.

- Exceptions show up late, so the team cleans up at the end.

That “cleanup culture” creates late nights and unstable financials. It also hides risk.

Objectives of Internal Controls

The objectives of internal controls guide what you build and what you test. In accounting, these objectives tie directly to close quality.

Core objectives of internal controls (accounting-relevant):

- Authorization: Only approved transactions post or pay.

- Completeness: You record everything that should be recorded.

- Accuracy: You record correct amounts, dates, and accounts.

- Validity/Occurrence: Transactions are real and supported.

- Safeguarding of assets: You protect cash, inventory, and data.

- Segregation of duties: No one person controls the full chain.

- Error handling & correction: You detect, resolve, and document issues.

How these objectives show up in month-end outcomes:

- Fewer late journal entries.

- Cleaner reconciliations.

- Fewer “why is this account off” conversations.

- Less rework and fewer review loops.

- A more predictable close calendar.

Why Are Internal Controls Important in Accounting?

The importance of internal controls in accounting comes down to trust. Your leaders, lenders, and owners rely on the numbers. Your team needs a close they can repeat.

Internal controls help you:

- Prevent and detect fraud. Deterrence works. People behave better with oversight.

- Improve financial statement reliability. You reduce late adjustments and restatements.

- Support compliance. Taxes, lender reporting, and regulated reporting all depend on clean data.

- Scale without heroics. You stop relying on one senior reviewer to catch everything.

- Reduce close stress. You move from late cleanup to early detection.

For example, I have seen teams “finish” the close and then discover a vendor master change caused duplicate payments. The team then reopens the period, reclasses entries, and reissues reports. One tight vendor-change control would have prevented days of rework.

Common “Symptoms” of Weak Controls (Diagnostic List)

These symptoms usually mean your accounting internal controls need attention:

- Reconciliations run late or vary by preparer.

- Balance sheet accounts carry old items with no owner.

- Journal entries lack support or show unclear approval.

- Vendor or customer master changes happen with no oversight.

- The close status stays unclear until the last few days.

- Reviewers find the same issues every month.

- Teams rely on Slack messages as “evidence.”

Internal Controls Framework in Accounting (COSO Explained for Practitioners)

COSO provides the most common internal controls framework accounting teams use. It gives you shared language and a practical structure.

The 5 Components of the COSO Framework (and What They Look Like in Accounting)

- Control Environment

You set expectations. You define roles. You enforce accountability. - Risk Assessment

You identify where errors or fraud could occur. You rank risks by impact and likelihood. - Control Activities

You run approvals, reconciliations, access controls, and reviews. - Information & Communication

You document what “done” means. You store evidence. You define escalation paths. - Monitoring Activities

You confirm controls happen on time and work as designed. You fix drift.

COSO → Month-End Close Reality

Types of Internal Controls in Accounting

Types of internal controls accounting teams use fall into a few practical buckets. You need a mix. One type never covers all risk.

Preventive vs. Detective vs. Corrective Controls

Preventive controls stop issues before posting or payment.

- Example: Dual approval for wires.

- Example: Required fields for vendor setup.

Detective controls find issues after they occur, but early.

- Example: Bank reconciliation with independent review.

- Example: Duplicate payment report.

Corrective controls fix root causes and prevent repeat issues.

- Example: Update approval thresholds after a miss.

- Example: Add a new close step for a recurring error.

Manual vs. Automated Controls

Manual controls work when you need judgment. They also break under pressure.

- Example: Flux review with commentary.

Automated controls work when rules stay consistent. They scale well.

- Example: System blocks posting without an approver.

Most teams run a hybrid. They automate what they can. They standardize the rest.

Entity-Level Controls vs. Process-Level Controls

Entity-level controls apply across the company.

- Example: Code of conduct and delegated authority policy.

- Example: Company-wide access review policy.

Process-level controls sit inside AP, AR, payroll, and close.

- Example: AP approval workflow.

- Example: Revenue cut-off checks.

Internal Controls Procedures in Accounting

Internal controls procedures accounting teams rely on look boring. They also prevent the most pain. You want them simple, repeatable, and time-bound.

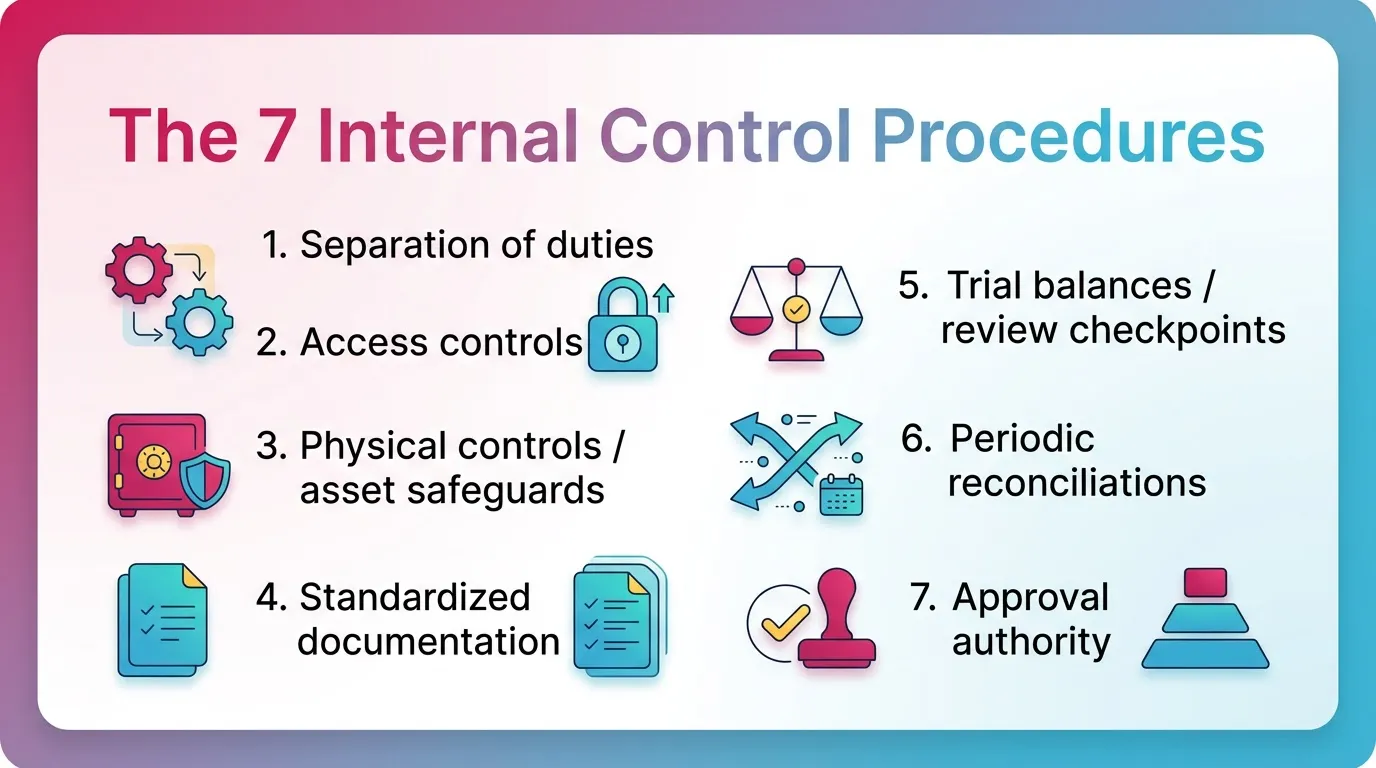

The 7 Internal Control Procedures

- Separation of duties

Split initiation, approval, processing, and reconciliation. - Access controls (systems + banking + vendor portals)

Use role-based access. Remove access fast after role changes. - Physical controls / asset safeguards

Protect checks, cash, inventory, and sensitive documents. - Standardized documentation

Use templates. Require support. Define minimum evidence. - Trial balances / review checkpoints

Add pre-close and close-stage reviews for key accounts. - Periodic reconciliations

Reconcile bank, AR, AP, and key balance sheet accounts on schedule. - Approval authority

Set thresholds. Define approvers. Document exceptions.

Internal Controls Examples in Accounting (By Process Area)

If you want internal controls examples accounting teams actually use, start with cash. Then cover AP, AR, payroll, journal entries, and reporting reviews.

Cash & Banking Controls (Highest Risk)

Cash moves fast. It also attracts fraud. Build strong controls here first.

- Bank rec monthly, completed by a set close day. Independent review required.

- Dual authorization for wires and ACH. No single-approver payments.

- Positive pay where possible.

- Restricted access to banking tokens and admin roles.

- Daily or weekly cash activity review. Focus on exceptions and new payees.

Accounts Payable (AP) Controls

AP creates both cash risk and expense misstatement risk.

- 3-way match when you use POs. Match PO, receipt, and invoice.

- Vendor onboarding approval workflow. Log changes to bank details.

- Duplicate payment detection. Review by vendor, amount, and invoice number.

- Approval thresholds by dollar amount and department.

- Restrict manual check runs and urgent wires.

Accounts Receivable (AR) Controls

AR controls protect revenue integrity and reduce write-off surprises.

- Credit memo approvals with clear reason codes.

- Separate cash application from AR write-offs.

- Aging review with dispute documentation and next steps.

- Revenue cut-off checks when timing matters.

- Lock down customer master changes.

Payroll Controls

Payroll touches sensitive data and creates high trust risk.

- Employee master file changes require approval.

- Separate HR changes from payroll processing.

- Payroll register review before release. Review variances and headcount.

- Bank account changes require verification steps.

Journal Entries & Close Controls

Journal entry controls protect the ledger from quiet errors.

- Journal entry templates with required support.

- JE approval routing based on materiality and risk.

- Standard month-end close checklist with sign-offs.

- Post-close review of top adjustments and recurring anomalies.

Financial Reporting Controls (P&L and Balance Sheet Review)

This is where many internal accounting controls either work or fail.

- Flux analysis for material accounts. Define thresholds.

- Balance sheet integrity checks. Tie-outs, agings, rollforwards.

- Reconciliation standards. Define what “complete” means.

- Review notes that explain what changed and why.

Internal Controls for Small Business Accounting

Internal accounting controls for small business teams must fit reality. Small teams cannot always segregate duties. However, you can still reduce risk.

The phrase “we’re too small for segregation of duties” can be true. It still does not remove the risk. It just changes your design.

Compensating controls for lean teams:

- Owner or partner reviews bank activity and new vendors weekly.

- Lock down permissions. Use read-only roles where possible.

- Have an outside bookkeeper or accountant review bank recs monthly.

- Use bank alerts for large payments and new payees.

- Require documented support for every manual JE.

Minimum viable control set for internal controls for small business accounting:

- Cash disbursements: dual approval or owner approval.

- Payroll: approved changes and register review.

- Close: bank rec plus key balance sheet reconciliations.

- Reporting: simple flux review for top accounts.

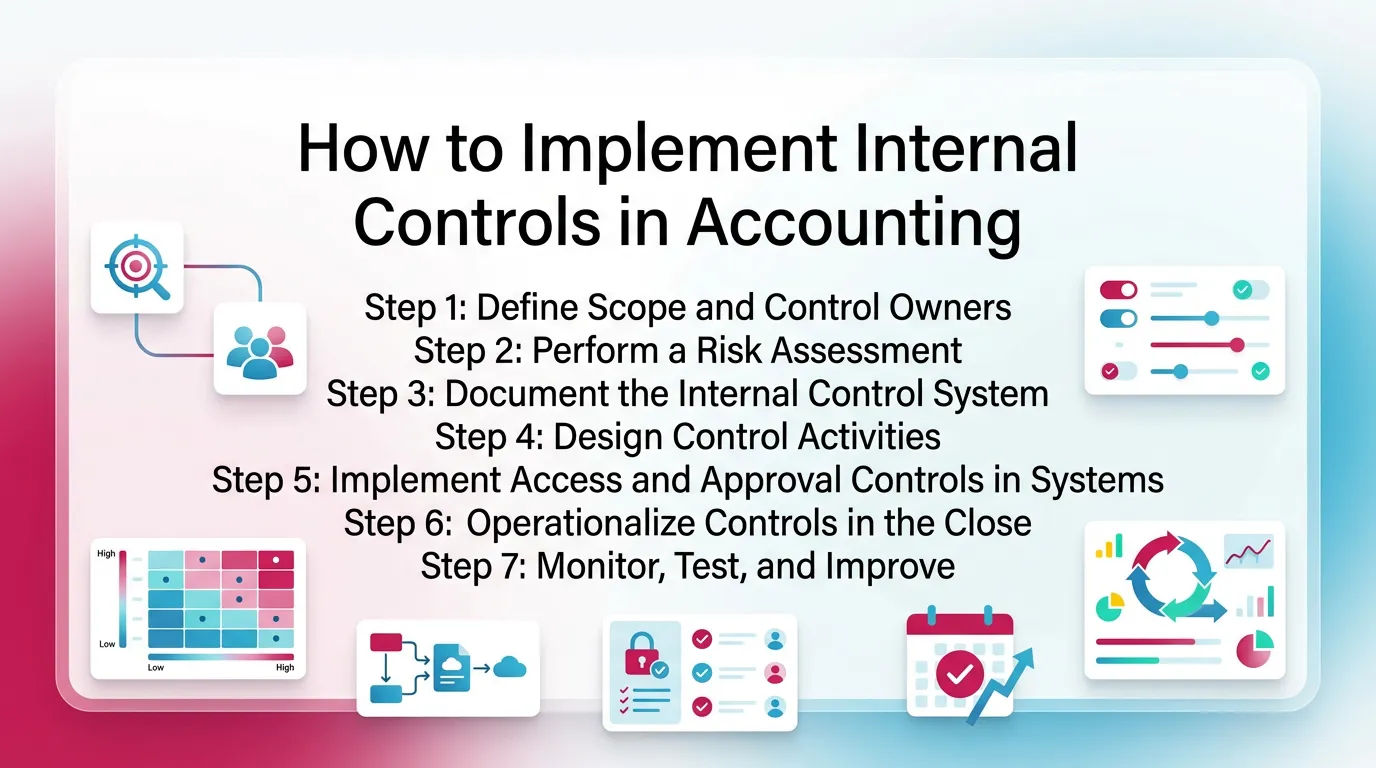

How to Implement Internal Controls in Accounting

How to implement internal controls in accounting? Start small, target risk, and embed controls in the close. Then monitor and improve.

Step 1: Define Scope and Control Owners

Define what you will control and who owns it.

- List processes: AP, AR, payroll, treasury, close, reporting.

- Identify critical accounts: cash, clearing accounts, AR, AP, payroll liabilities.

- Assign owners:

- Preparer completes the work.

- Reviewer checks and signs off.

- Approver authorizes high-risk actions.

Tip from practice: write names, not titles. Titles change. Names create clarity.

Step 2: Perform a Risk Assessment

Identify what can go wrong and where it will hurt.

- Rate risks by impact and likelihood.

- Tie each risk to assertions:

- Completeness

- Accuracy

- Occurrence/validity

- Cut-off

- Prioritize cash and vendor changes early.

A practical approach: start with last quarter’s “surprise list.”

If it surprised you, it needs a control.

Step 3: Document the Internal Control System

Documentation turns tribal knowledge into a repeatable system.

- Define policies, thresholds, and evidence requirements.

- Standardize naming for support files.

- Define where evidence lives and how long you keep it.

Keep it short. One page per process often works.

Step 4: Design Control Activities

Match control design to risk.

- Choose the control type and frequency.

- Define acceptance criteria. Define what triggers an exception.

- Make the review step specific:

- “Review AP” fails.

- “Review AP aging for items over 60 days and explain” works.

Step 5: Implement Access and Approval Controls in Systems

Lock down access and route approvals in the tools you already use.

- Use role-based permissions in your GL system.

- Restrict vendor and bank detail changes.

- Control bill pay tools and banking roles.

- Document override rules and who can approve overrides.

Step 6: Operationalize Controls in the Close

Controls must live inside the monthly close sequence.

- Put controls on the close calendar.

- Assign due dates by close day, not by “end of month.”

- Keep evidence capture simple and consistent.

- Tie exceptions to tasks so they get resolved.

This is where many teams win or lose. A control that happens late acts like a report, not a control.

Step 7: Monitor, Test, and Improve

Controls drift over time. People change. Systems change. Volume changes.

- Check timeliness. Check completeness. Check quality.

- Track exceptions and remediation. Fix root causes.

- Refresh thresholds at least annually.

A simple monitoring rhythm:

- Monthly: missed control log.

- Quarterly: access review.

- Semi-annual: control design review.

Internal Controls Checklist Accounting (Copy/Paste Template)

Use this internal controls checklist accounting template as a starting point. Add owners, dates, and evidence standards.

Master Checklist

Evidence Standards

Save evidence that proves the control happened and that the reviewer made a decision.

- Reconciliation support and tie-outs

- Approval logs and routing history

- Exception notes and follow-up actions

- Reviewer sign-off with date

- Supporting reports used in the review

Best Practices for Internal Controls in Accounting

These practices keep accounting internal controls working during busy closes.

- Design controls around where errors appear. Focus on cash, vendor changes, and unsupported JEs.

- Use standard review logic. Do not rely on reviewer preference.

- Shift from checklist completion to exception-driven review.

- Keep controls time-bound with close day targets.

- Treat documentation as part of the control. Evidence proves effectiveness.

One practical example: define a flux threshold and stick to it.

For example, “Investigate any P&L variance over 10% and $10,000.”

That one rule improves consistency across reviewers.

Common Mistakes

- You rely on segregation of duties without monitoring. People still collude or override.

- Controls exist on paper but not in the close workflow. They get skipped.

- You use no consistent thresholds. Reviews become subjective.

- Reviews happen too late. You find issues after reports go out.

- Evidence capture stays weak. You cannot prove the control happened.

How Modern Teams Operationalize Accounting Controls With Xenett (Without Turning It Into “More Admin”)

Many breakdowns happen during account-level review in close. The work becomes manual, inconsistent, and late. Xenett helps teams run internal controls in accounting with more structure and visibility.

Xenett is not an audit tool and does not provide audit services. It supports close execution and accounting review workflows.

Review-First Control Execution (P&L + Balance Sheet)

Xenett supports structured account-level review. It helps teams surface anomalies earlier.

- Highlight unusual flux and unexpected balances.

- Spot missing entries and reconciliation gaps.

- Standardize review steps across staff and across clients.

This makes controls repeatable. It reduces “it depends who reviewed it.”

Related Xenett resource: https://xenett.com/blog/month-end-close-checklist/

Close Task and Checklist Management (Control Completion With Accountability)

Xenett connects review findings to work that resolves them.

- Tie exceptions to specific tasks and owners.

- Track due dates by close day.

- Reduce box-checking by linking tasks to accounts and issues.

Review and Approval Workflows (Evidence + Sign-Off Discipline)

Xenett supports consistent sign-offs without adding heavy admin.

- Show who reviewed what and when.

- Keep notes tied to accounts and periods.

- Keep decisions and follow-ups easy to find.

This creates a clearer trail of review decisions. It also supports continuity when staff changes.

Visibility Into Close Status and Bottlenecks

Xenett improves visibility into what blocks the close.

- Identify reconciliation lag early.

- See unresolved flux items before the final days.

- Manage sequencing so controls happen at the right time.

FAQ: Internal Controls in Accounting

What are internal controls in accounting?

Internal controls in accounting are the policies, procedures, and checks used to help ensure transactions are authorized, recorded accurately, assets are safeguarded, and financial reporting is reliable and compliant.

What are examples of internal controls in accounting?

Examples of internal controls in accounting include segregation of duties, access controls, reconciliations, approval authority, standardized documentation, transaction reviews, and automated system checks.

What are the 5 main internal controls?

The five components in the internal controls framework accounting teams often use (COSO) are Control Environment, Risk Assessment, Control Activities, Information & Communication, and Monitoring Activities.

What are the 7 internal control procedures?

The seven internal controls procedures accounting teams rely on are separation of duties, access controls, physical controls, standardized documentation, trial balance and review checkpoints, periodic reconciliations, and approval authority.

What are the objectives of internal controls?

Objectives of internal controls include authorization, completeness, accuracy, validity/occurrence, safeguarding of assets, segregation of duties, and effective error handling and correction.

How do you implement internal controls in accounting?

Define scope and owners, perform a risk assessment, document what “done” means, design preventive and detective controls, embed them in the monthly close, and monitor effectiveness over time.

What internal controls should a small business prioritize first?

Internal accounting controls for small business should start with cash controls. Add bank recs with review, payment approvals, vendor-change oversight, basic access restrictions, and monthly balance sheet reconciliations.

Are internal controls the same as an audit?

No. Internal controls are your internal processes to reduce risk and improve reliability. An audit is an examination that may evaluate those controls. Controls should exist even without an audit.

Conclusion

Internal controls accounting works best when you build it into the close. Start with cash, vendor changes, and account-level review. Define owners and evidence. Keep controls time-bound and repeatable.

If you want to strengthen your internal control system in accounting, pick three high-risk controls and implement them this month. Then expand each close until your checklist becomes routine.

Use the internal controls checklist accounting section above to start. Assign owners today. Set close-day deadlines. Save evidence as you go.

.webp)