.svg)

What Is a Bank Reconciliation? Meaning, Purpose, and Examples

Blog Summary / Key Takeaways

- The bank reconciliation meaning stays simple. Prove your Cash GL ties.

- A strong bank reconciliation definition includes support and review.

- Most differences come from timing or missing book entries.

- You should not “force match” to make it reconcile. Fix the cause.

- Tight recons speed up the close and reduce cash surprises.

- Tools help, but review controls still matter.

What Is a Bank Reconciliation?

Bank Reconciliation Meaning

Bank reconciliation means proving the cash balance in your books agrees

to the cash balance at the bank, after known differences.

That sounds simple. In practice, it protects the most used number

in your financials. Cash drives decisions fast.

Bank Reconciliation Definition

A bank reconciliation is an internal control. You compare bank activity

to book activity so you can verify cash activity is complete and accurate.

It helps you:

- identify items the bank recorded that you did not record in the GL

- identify items you recorded that the bank has not cleared yet

- correct errors and document reconciling items

If you manage multiple entities or many clients, this control matters more.

Small errors multiply across accounts and periods.

Bank Reconciliation vs. Reconciliation of Bank Statement

Most people use both phrases the same way. “Reconciliation of bank statement”

usually means the bank rec.

However, the goal is not just checking the statement.

The goal is supporting the Cash account in the GL.

The statement acts as evidence. Your GL acts as the system of record.

Your reconciliation connects them with explanations you can defend.

Bank Reconciliation in Accounting: Where It Fits in Month-End Close

What Account Is Being Reconciled?

You reconcile balance sheet cash accounts. These often include:

- operating checking

- savings accounts

- payroll accounts

- merchant clearing accounts

- trust accounts, if applicable

Cash affects P&L, too. Banks post fees, interest, and chargebacks.

Those items must hit the right income or expense accounts.

Why Bank Reconciliation Is a Foundational Control

If cash is wrong, your close becomes unstable. Every cash-driven tie-out

gets harder and slower.

For example, I have seen teams chase an AR variance for hours.

A single bank chargeback caused it. The bank rec would have flagged it.

Cash errors also break:

- clearing accounts

- undeposited funds

- merchant processor reconciliations

- debt covenant reporting, when relevant

Therefore, you should treat cash as an early close gate.

Do not push it to the end.

When Is a Bank Reconciliation Performed?

Most businesses reconcile monthly. That matches the close cycle.

Some accounts need more:

- weekly or daily for high volume

- weekly for fraud risk or cash tightness

- daily for payment processors, in some models

You should finish the bank rec before final close sign-off.

You should not finalize financials with unreconciled cash.

Who Typically Does Bank Reconciliations?

Roles vary by size and risk:

- bookkeeper or staff accountant prepares

- senior accountant or controller reviews

- firm owner or CAS leader sets standards across clients

Separation of duties helps. The person who approves payments

should not also “finalize” the bank rec without review.

Why Bank Reconciliation Is Important

Purpose of Bank Reconciliation

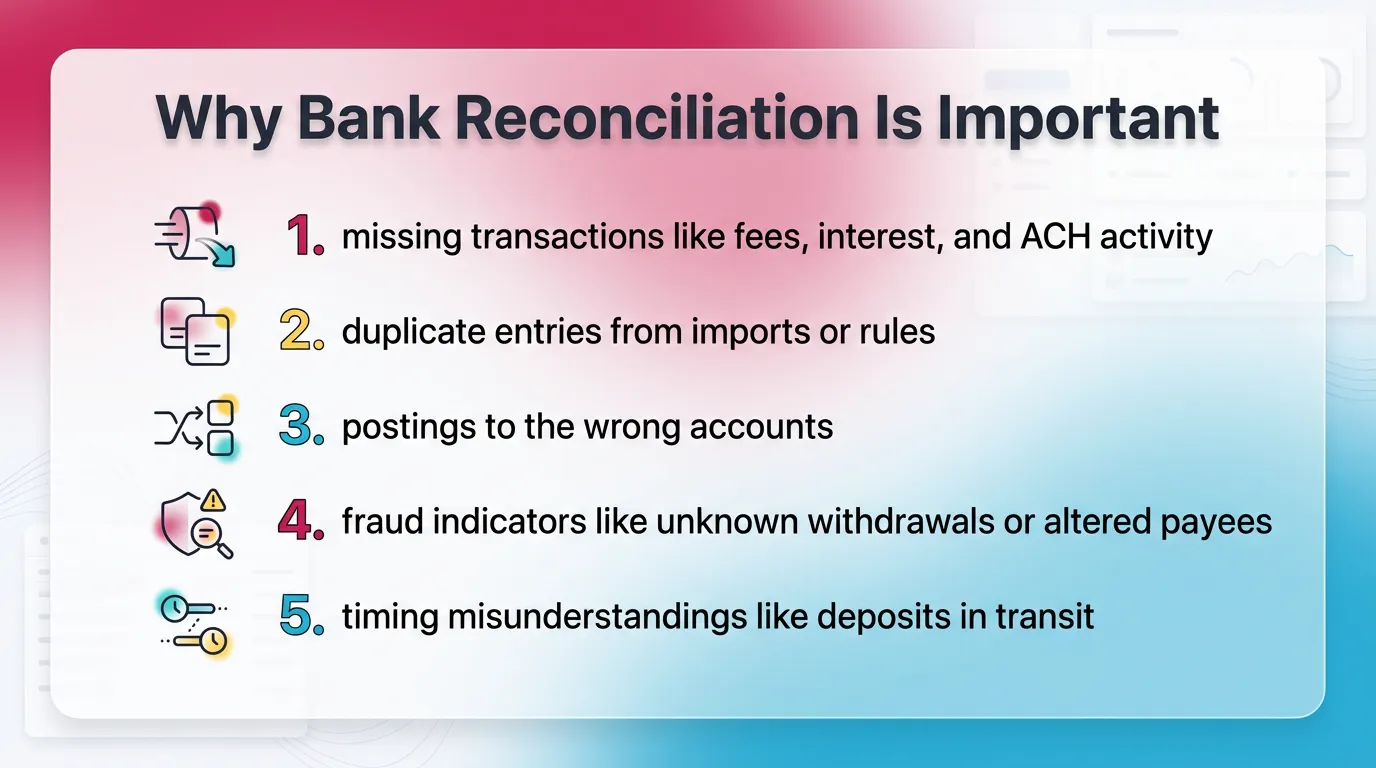

The purpose of bank reconciliation is cash integrity. It catches issues

before they become reporting problems.

It prevents or catches:

- missing transactions like fees, interest, and ACH activity

- duplicate entries from imports or rules

- postings to the wrong accounts

- fraud indicators like unknown withdrawals or altered payees

- timing misunderstandings like deposits in transit

It also forces discipline around documentation.

That makes close review faster.

Practical Business Outcomes (What Improves When Recons Are Tight)

When you reconcile well, you get:

- a reliable cash position for decisions

- a faster and calmer close

- a cleaner audit trail for internal review and lenders

- fewer surprises in monthly financial review

What Causes Differences Between Bank Balance and Book Balance?

Common Reconciling Items

Most differences fall into a few buckets. You should expect them.

You should still support and age them.

Here are the common reconciling items.

Checks Outstanding Bank Reconciliation: What It Means

In a checks outstanding bank reconciliation, an outstanding check means

you recorded the check, but the bank has not cleared it yet.

It is a timing difference. It does not mean missing cash.

You should make outstanding checks traceable with:

- check number

- payee

- issue date

- amount

- reason it remains outstanding

You should review staleness monthly.

Old checks can signal:

- a vendor never received the check

- a duplicate payment risk

- a void and reissue need

- an address or payee issue

In real workflows, this is where teams get stuck.

They “roll” old checks for months. That hides risk.

Bank Reconciliation Statement: What “Good” Looks Like

What a Bank Reconciliation Statement Usually Includes

A good bank reconciliation statement shows the tie-out clearly.

It also shows who did the work and who reviewed it.

It usually includes:

- statement ending balance

- plus or minus reconciling items

- adjusted bank balance

- book ending balance

- adjustments required to books, if any

- prepared-by and reviewed-by evidence, with dates

This structure works whether you use spreadsheets or software.

It also supports consistent file review.

Documentation Standards (EEAT + Control Lens)

A clean recon needs more than a tie number. It needs evidence.

Each reconciling item should be:

- supported with a source and reference

- explained in plain English

- aged, with days outstanding

- dispositioned, with next action and owner

This helps in real life. People change roles. Clients change staff.

Your documentation becomes the memory of the close.

Bank Reconciliation Example

Simple Example Scenario (Numbers Only)

- Bank statement ending balance: $25,000

- Book cash balance: $26,200

- Differences identified:

- Outstanding check: $1,500

- Bank fee not recorded: $20

- Deposit in transit: $1,720

What This Example Demonstrates

This bank reconciliation example shows two types of differences.

Timing items:

- deposit in transit

- outstanding check

Book entry items:

- bank fee not recorded

A matched reconciliation means you explain differences and support them.

You do not ignore them. You do not bury them in misc accounts.

If your team reviews cash fluctuations each month, this example helps.

Bank fees often explain “why cash moved” without an obvious invoice.

Bank Reconciliation Journal Entries

You post entries when the bank records activity you missed.

You also post entries when you find book errors.

Keep entries simple. Add memos. Attach support when possible.

This improves review speed later.

Typical Entries Triggered by Reconciliation Findings

Common bank reconciliation journal entries example types include:

- Bank fees:

- Debit Bank Fees Expense

- Credit Cash

- Interest earned:

- Debit Cash

- Credit Interest Income

- NSF / returned deposit:

- Debit Accounts Receivable (or relevant account)

- Credit Cash

- Corrections for book errors:

- reclass entry or amount correction

- include memo and source support

You should also consider tax coding where needed.

For example, fees may map differently by entity type.

Best Practices for Bank Reconciliations

A Bank Reconciliation Checklist

You can standardize quality without turning it into busywork.

Use a short checklist that protects cash.

A strong checklist includes:

- confirm statement period and cutoff match the close period

- confirm you reconcile the correct account and bank login

- ensure each reconciling item has support and an owner

- age outstanding items and review old items monthly

- require prepared-by and reviewed-by sign-off

- keep coding consistent for bank-originated items

- tie completion to close readiness

This also supports bank reconciliation services in a firm.

Clients expect consistency across accounts and months.

If you train staff, you can also use bank reconciliation practice problems.

Give them a sample statement, a messy GL, and clear expectations.

Then grade for documentation, not just the final tie number.

Common Mistakes (And Why They Create Cleanup Later)

.webp)

Teams often struggle for predictable reasons.

Common mistakes include:

- treating the bank rec like a box-check task

- letting reconciling items roll forward without aging

- posting adjustments with no explanation

- reconciling to the wrong statement or wrong account

- force-matching to clear differences

Force-matching creates false comfort. It hides root causes.

It also makes future periods harder.

When you see recurring issues, fix the upstream process.

For example:

- tighten bank feed rules

- reduce manual entries

- standardize merchant clearing workflows

How Xenett Supports Repeatable Bank Reconciliation Standards Across the Close

Bank Reconciliation Is Only “Done” When Review Is Done

Bank reconciliation often “finishes” in the GL. Review does not always follow.

That gap causes late surprises.

Xenett helps teams structure account-level review.

It helps cash issues surface earlier in the close.

This matters when:

- cash swings look unusual

- reconciling items linger

- fees and interest get coded inconsistently

- NSF items sit without follow-up

Close Task and Checklist Management (So Cash Doesn’t Slip)

Cash should not disappear inside someone’s inbox.

Xenett helps standardize close checklists.

It makes bank reconciliations required and visible per entity.

This supports consistent execution across:

- multi-entity businesses

- accounting teams with handoffs

- firms managing many clients

Review and Approval Workflows

Preparation does not equal completion. Review must confirm quality.

Xenett supports clear prepared-by and reviewed-by workflows.

It helps teams enforce the pattern:

reconcile → review findings → resolve → approve.

Therefore, you reduce “done but not reviewed” close risk.

You also coach staff faster with consistent feedback.

Visibility Into Close Status and Bottlenecks

In real closes, the issue is not knowing cash matters.

The issue is losing track of where cash stands.

Xenett gives visibility into:

- which accounts remain unreconciled

- which recons wait on review

- what blocks completion, with notes and context

This helps controllers manage the close in minutes.

It also helps firms manage client work at scale.

FAQ

What Is a Bank Reconciliation?

Bank reconciliation is the process of comparing bank statement activity to your

accounting records to ensure cash balances match and to explain differences.

It confirms your Cash GL is complete and accurate.

It also documents reconciling items.

What Is the Purpose of Bank Reconciliation?

The purpose of bank reconciliation is to keep cash accurate.

It identifies timing differences, missing entries, and errors.

It also supports clean financial reporting.

It reduces late close cleanup.

Why Is Bank Reconciliation Important?

Why bank reconciliation is important comes down to trust in cash.

It reduces errors, helps detect fraud, and prevents surprises in review.

It also supports lenders, owners, and managers who rely on cash.

Cash drives fast decisions.

When Should Bank Reconciliations Be Done?

Most businesses do bank reconciliations monthly.

Higher-volume or higher-risk accounts often need weekly or daily recs.

You should complete them before final close approval.

Do not finalize with unreconciled cash.

What Are Outstanding Checks in a Bank Reconciliation?

Outstanding checks are checks recorded in the books that have not cleared the

bank yet. They are timing differences.

Track them by check number and age.

Review stale checks each month.

Is Bank Reconciliation the Same as Reconciling a Bank Statement?

In casual usage, yes. People say “reconciliation of bank statement.”

In accounting, you reconcile the Cash account in the GL to the bank’s record.

The statement provides evidence.

The GL needs to be correct.

What Journal Entries Commonly Come From Bank Reconciliations?

Common entries include bank fees, interest earned, NSF items, and corrections

for miscoded or duplicate transactions.

Add clear memos and support.

That speeds review and reduces rework.

What Is Bank Reconciliation Software?

Bank reconciliation software helps match bank transactions to book

transactions. It flags exceptions and supports documentation and review.

It reduces manual matching time. It does not remove the need for review.

What Is Automated Bank Reconciliation?

Automated bank reconciliation uses rules and matching logic to auto-match

transactions and surface exceptions.

It works best with consistent payees and amounts.

You still need accounting judgment on exceptions.

How Do You Undo a Bank Reconciliation in QuickBooks Online?

How to undo bank reconciliation in QuickBooks Online depends on your

permissions and the period. You often must adjust reconciled transactions

or use accountant tools.

QuickBooks changes features over time.

Use an accountant-led process to avoid breaking prior periods.

How to Reconcile a Bank Statement

How to reconcile a bank statement means you match bank activity to your

book activity, then explain what does not match.

You confirm cutoff, clear matches, and document reconciling items.

Then you post needed book entries and complete review.

If you use QuickBooks, people also search:

- quickbooks reconciliation

- how to reconcile in quickbooks

- quickbooks bank reconciliation

Those workflows differ by version.

However, the control goal stays the same.

Conclusion

A bank reconciliation protects the number everyone uses first. Cash.

It also stabilizes your month-end close.

Set a standard for support, aging, and review. Then enforce it every month.

If you want tighter execution, build cash reconciliations into your close plan

and review workflow in Xenett, so prep and review stay visible and consistent.