.webp)

.svg)

Prepaid Expenses in Accounting: What They Are, How to Record Them, and How to Manage Them

.jpg)

Blog Summary / Key Takeaways

• Prepaid expenses are payments made in advance for goods or services not yet received

• They are recorded as current assets on the balance sheet, not as expenses at the time of payment

• The expense is recognized gradually as the benefit is consumed, typically through monthly amortization

• Common examples: insurance, rent, software subscriptions, retainers, and maintenance contracts

• Mishandling prepaid expenses is one of the most common balance sheet errors in small business books

• A prepaid schedule tracks each prepaid, its total amount, monthly expense, and remaining balance

Most bookkeeping errors are not dramatic. They do not show up as missing invoices or obvious fraud.

They show up as a $12,000 insurance premium that got expensed in January instead of spread across 12 months. The P&L looks terrible in January and suspiciously good in February through December. The balance sheet has no prepaid asset. And the client thinks their profitability is more volatile than it actually is.

Prepaid expenses are one of the most commonly mishandled items in small business bookkeeping. This guide explains what they are, how to record them correctly, and how to manage them at scale.

What Are Prepaid Expenses?

A prepaid expense is a payment made in the current period for a benefit that will be received in a future period.

When you pay for something before you use it 12 months of insurance up front, six months of rent in advance, an annual software subscription that payment is not an expense yet. It is an asset. You have paid for something of value that you have not yet consumed.

Under accrual accounting, expenses are recognized when they are incurred when the benefit is consumed not when the cash is paid. That is the core principle that makes prepaid expense accounting necessary.

Common Examples of Prepaid Expenses

How to Record a Prepaid Expense: The Journal Entries

There are two journal entries involved in prepaid expense accounting: the initial payment and the monthly amortization.

Step 1: Record the initial payment

When the payment is made, debit the Prepaid Expense account (an asset) and credit Cash or Accounts Payable.

This records the payment as an asset money spent on a future benefit not as an expense.

Step 2: Record monthly amortization

At the end of each month, recognize the portion of the prepaid that was consumed. For a $12,000 annual insurance premium, that is $1,000 per month.

This entry reduces the asset balance and recognizes the expense in the correct period. After 12 months, the prepaid account balance is zero and the full $12,000 has been expensed one month at a time.

Prepaid Expenses on the Balance Sheet

Prepaid expenses appear in the current assets section of the balance sheet, below cash and receivables but above inventory and other current assets.

The balance represents the amount of prepaid benefit remaining the value of what has been paid for but not yet consumed.

A balance sheet with no prepaid expenses for a business that pays annual insurance or rent in advance is a sign that payments are being expensed immediately rather than deferred. That is one of the most common bookkeeping errors in small business books.

The Prepaid Expense Schedule

Managing multiple prepaid items manually is error-prone. A prepaid schedule tracks every active prepaid in one place and makes monthly amortization mechanical rather than dependent on memory.

At the end of each month, the bookkeeper posts amortization entries for each line on the schedule and updates the remaining balance. The total of all remaining balances should tie to the Prepaid Expenses account on the balance sheet.

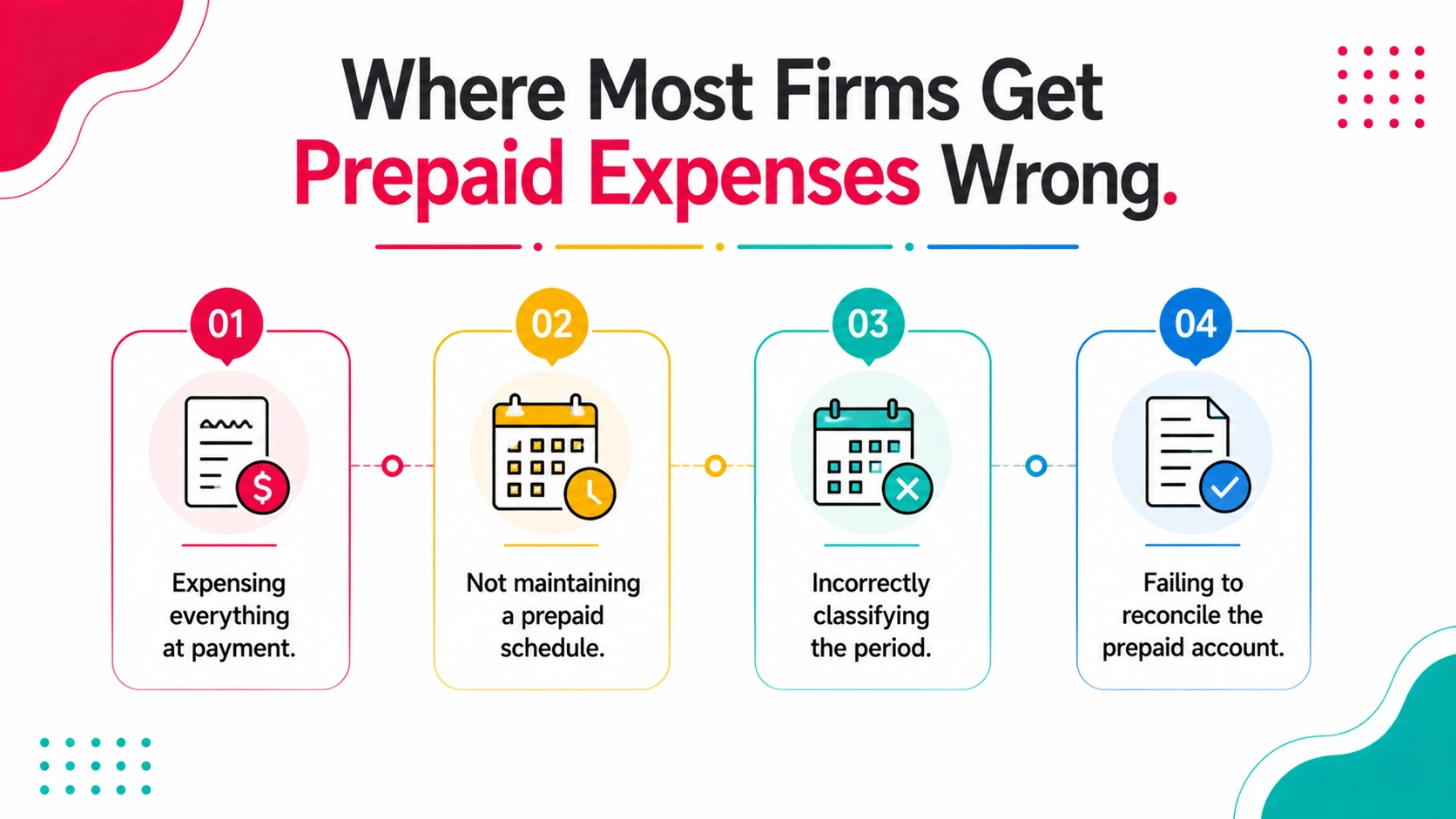

Where Most Firms Get Prepaid Expenses Wrong

After working with 1,000+ accounting firms, these are the most consistent prepaid expense errors.

Expensing everything at payment.

The most common error. A $9,000 annual software subscription hits the P&L in full in January. The next 11 months show no software expense. Margins look wrong in both directions.

Not maintaining a prepaid schedule.

Without a schedule, amortization depends on someone remembering to post it each month. When they forget or when they leave the entries stop and the balance sheet balance grows without matching the reality of what has been consumed.

Incorrectly classifying the period.

A December insurance payment for a January to December policy should be a prepaid at December 31. Many bookkeepers expense it in December because that is when the check was written.

Failing to reconcile the prepaid account.

The Prepaid Expenses balance on the balance sheet should always tie to the sum of remaining balances on the prepaid schedule. If it does not, something has been posted incorrectly or an entry was missed.

Real Scenario: A $14,000 Balance Sheet Error from Missed Amortization

A small CPA firm took over the books for a medical practice client. On the first balance sheet review, the Prepaid Expenses account showed $14,000.

After pulling the prepaid schedule which had not been updated in five months the team found that five months of amortization entries had not been posted. The prior bookkeeper had set up the schedule correctly in January but stopped posting monthly entries in March.

The balance sheet was overstating assets by $14,000. More importantly, five months of insurance and rent expense had been missing from the P&L. The income statement had been overstating profit.

Correcting it required five months of catch-up journal entries and a revised P&L. It took four hours to fix. Monthly amortization entries take five minutes.

How Xenett Can Help

Xenett's Close Dashboard includes status tracking for balance sheet reconciliation including prepaid expense accounts. Firms that use Xenett can track whether the prepaid account has been reconciled for each client at month end, visible across the entire client base in one screen.

• Close Dashboard: see which clients have reconciled prepaid accounts and which have open items

• Recurring task automation: monthly amortization entry tasks auto-generate on schedule for every client

• Review workflows: prepaid schedule review is a tracked step in the close workflow not something that gets skipped

• Document management: prepaid schedules stored and versioned alongside other close documentation

Book a demo at xenett.com/demo to see how Xenett supports balance sheet reconciliation at scale.

FAQs

What are prepaid expenses in accounting?

Prepaid expenses are payments made in the current period for benefits to be received in future periods. They are recorded as current assets on the balance sheet and expensed gradually as the benefit is consumed.

Are prepaid expenses an asset or an expense?

At the time of payment, they are an asset, Prepaid Expenses on the balance sheet. They become an expense over time as the benefit is consumed through monthly amortization journal entries.

How are prepaid expenses recorded in QuickBooks?

In QBO, create a current asset account called Prepaid Expenses (or separate accounts per type: Prepaid Insurance, Prepaid Rent, etc.). Record the initial payment as a debit to the prepaid account. Each month, post a journal entry debiting the relevant expense account and crediting the prepaid account for the monthly amortization amount.

What is the difference between prepaid expenses and accrued expenses?

Prepaid expenses are cash paid before the benefit is received an asset. Accrued expenses are costs incurred before cash is paid a liability. Both are tools for matching expenses to the period in which they are incurred.

How long do prepaid expenses stay on the balance sheet?

Until the benefit is fully consumed. A 12-month insurance policy paid in January will have a declining balance each month for 12 months and reach zero at the end of December.

What accounts are affected by prepaid expenses?

Two accounts: Prepaid Expenses (a current asset) and the relevant expense account (Insurance Expense, Rent Expense, etc.). The initial payment also affects Cash or Accounts Payable.

Can prepaid expenses be long-term assets?

If the prepaid period extends beyond 12 months, the portion beyond 12 months should be classified as a long-term or non-current asset. The current portion (next 12 months) stays in current assets.

Conclusion

Prepaid expenses are not complicated. The concept is simple: pay now, expense later.

The execution is where most bookkeepers get it wrong, not because the process is hard, but because it requires consistent monthly attention and a schedule to track it.

A maintained prepaid schedule, monthly amortization journal entries, and a balance sheet reconciliation at month end are all it takes to get this right. And getting it right means accurate P&Ls, accurate balance sheets, and clients who can trust the numbers.

See how Xenett's close workflow supports balance sheet reconciliation across your client base: xenett.com/demo

Prepaid expenses are payments made in the current period for benefits to be received in future periods. They are recorded as current assets on the balance sheet and expensed gradually as the benefit is consumed.

At the time of payment, they are an asset Prepaid Expenses on the balance sheet. They become an expense over time as the benefit is consumed through monthly amortization journal entries.

In QBO, create a current asset account called Prepaid Expenses (or separate accounts per type: Prepaid Insurance, Prepaid Rent, etc.). Record the initial payment as a debit to the prepaid account. Each month, post a journal entry debiting the relevant expense account and crediting the prepaid account for the monthly amortization amount.

Prepaid expenses are cash paid before the benefit is received an asset. Accrued expenses are costs incurred before cash is paid a liability. Both are tools for matching expenses to the period in which they are incurred.

Until the benefit is fully consumed. A 12-month insurance policy paid in January will have a declining balance each month for 12 months and reach zero at the end of December.

Two accounts: Prepaid Expenses (a current asset) and the relevant expense account (Insurance Expense, Rent Expense, etc.). The initial payment also affects Cash or Accounts Payable.