.webp)

.svg)

Accrual Accounting Explained: Definition, Examples, and Key Differences

.jpg)

Key Takeaways

- Accrual accounting definition: Records revenue when earned and expenses when incurred, regardless of when cash moves.

- Why it’s used: Produces a more accurate period-by-period picture of performance and obligations.

- Most common accruals: Accrued expenses, accrued revenue, prepaid expenses, deferred revenue.

- Cash vs accrual: Cash tracks payment timing; accrual tracks economic activity timing.

- Where it shows up: Month-end close, revenue recognition, AP/AR, and financial reporting.

What Is Accrual Accounting?

Accrual Accounting

Accrual accounting records revenue when you earn it and expenses when you incur them. Cash timing does not control the entry. That is the accrual accounting definition most teams use for close and reporting.

It’s accounting based on when work happens, not when money hits the bank.

If someone asks, “what is accrual accounting,” this is the core idea. You align activity to the right period. Therefore your monthly financials mean more.

What Does “Accrual” Mean in Accounting?

In plain terms, what does accrual mean in accounting? It means you record something now because it belongs to this period. You often record it before you pay cash or receive cash.

So what is an accrual in accounting? It is a timing entry. It moves revenue or expense into the correct month.

Here is the key split:

- Accruals = timing adjustments in the books.

- Cash transactions = money movement in the bank.

Cash still matters. However accruals explain performance. They also explain what you owe and what customers owe you.

What Is Accrual Basis Accounting?

Accrual basis accounting uses accruals as the default. You recognize revenue when earned. You recognize expenses when incurred.

So what is accrual basis accounting used for? It supports financial reporting and management reporting. It also supports better forecasting inputs.

You may also see these phrases:

- what is accrual based accounting

- what is accrual basis of accounting

They all point to the same method. Many lenders and investors expect accrual-basis financials. Most accounting teams also prefer it for month-end decisions.

How Accrual Accounting Works

The Two Rules That Drive Accrual Accounting

Accrual accounting follows two rules:

- Recognize revenue when earned. You earn it when you deliver the product or service.

- Recognize expenses when incurred. You incur them when you receive the benefit or create the obligation.

These rules sound simple. The hard part is cut-off. That is why month-end discipline matters.

The Matching Principle

Accrual accounting exists to match cause and effect in the same period. When you book revenue, you also book the related costs in that same window.

This improves how period profitability reads. It reduces noise from random payment timing. Therefore your margin trends tell a clearer story.

If you manage a team, you have seen this. A late vendor bill can flip a month from “great” to “bad.” Accruals prevent that surprise.

Where Accruals Live on the Financial Statements

Accruals hit the balance sheet first. Then they flow into the income statement as you recognize revenue or expense.

Common balance sheet accounts affected:

- Accounts receivable (AR)

- Accounts payable (AP)

- Accrued liabilities

- Prepaid expenses

- Deferred (unearned) revenue

Income statement impact:

- Revenue timing

- Expense timing

Transaction → Accrual Entry → Financial Statement Impact

Accrual Accounting Examples

Quick Examples

Here are four accrual accounting example situations you will see in real closes:

- Accrued expense example: Utilities used in December. Invoice gets paid in January.

- Accrued revenue example: You deliver services in December. You bill and collect in January.

- Prepaid expense example: You pay insurance up front. You expense it monthly.

- Deferred revenue example: You collect subscription cash now. You recognize revenue over time.

These examples show the same point. Accrual accounting follows the work, not the cash.

Expanded Example: A Month-End Timeline

Accrual accounting pulls activity into the month it belongs to. This timeline shows it across two months.

Example 1: Sale on credit (AR + revenue)

- December 28: You deliver $10,000 of services. You have not billed yet.

- December 31 close: You book revenue and AR (or unbilled).

- January 5: You send the invoice.

- January 20: Customer pays. You clear AR.

Example 2: Wages earned but not yet paid (accrued payroll)

- Dec 23–Dec 31: Staff earns $8,000 in wages.

- December 31 close: You book wages expense and wages payable.

- January 6: You run payroll. You clear wages payable.

Common Types of Accruals (With Risks)

This table helps reviewers spot what breaks.

Real-world insight from close work: payroll and revenue cut-off create most churn.

They also create most rework. You can reduce both with a fixed close calendar.

Accrual vs. Cash Accounting

Accrual vs Cash Accounting: Side-by-Side Comparison

Accrual vs cash accounting comes down to timing. Cash follows payments. Accrual follows earned and incurred activity.

Here is a side-by-side view for cash vs accrual accounting.

People often search “accrual accounting vs cash accounting” when results look odd.

The table above usually explains why.

When Cash Basis Looks “Simpler”

Cash basis feels easier because it avoids accrual journal entries. However it can hide real performance.

Common distortions:

- Revenue spikes because collections hit in one month.

- Expense dips because bills stay unpaid at month-end.

- “Profit” looks strong right before large payments clear.

That distortion hurts decisions. It can mislead on:

- Gross margin trends

- Hiring capacity

- Runway and burn

- Department budgets

If you report to leadership, this becomes a trust issue. Leaders want stable signals.

Accrual accounting gives them that stability.

When Accrual Accounting Is Usually Preferred

Accrual accounting becomes more useful as operations get real.

Common triggers:

- You invoice multiple customers each month (AR).

- You receive vendor bills after month-end (AP cut-off).

- You sell subscriptions, retainers, or prepaid packages.

- You manage inventory or track COGS.

- You need credible monthly reporting for owners or lenders.

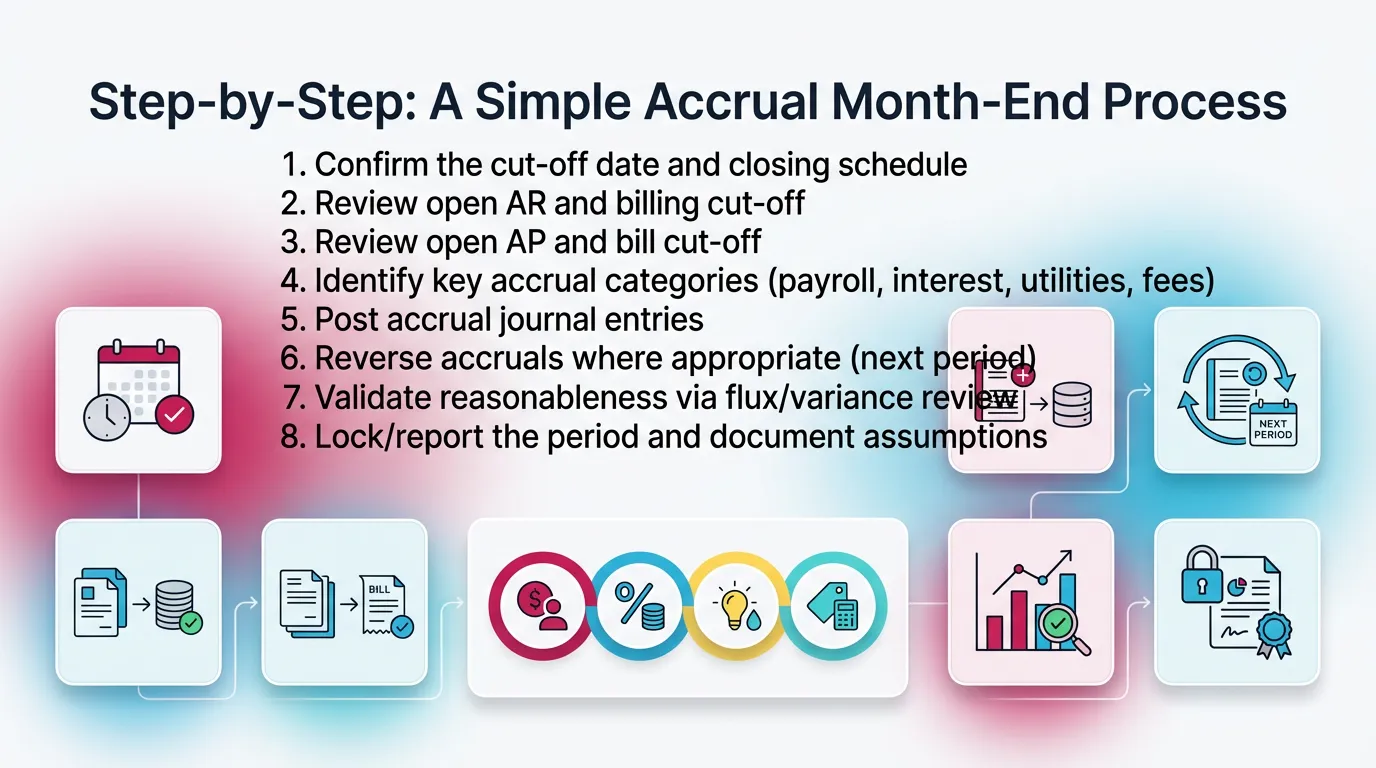

The Accrual Accounting Method: What Gets Adjusted at Month-End?

The accrual accounting method adds entries at month-end to fix timing. These entries capture unrecorded earned revenue and incurred costs. They also spread prepaids and deferred revenue across periods.

If you ask, what is the accrual method of accounting, this is the practical answer.

It is a system of cut-off and adjustments that make monthly reporting reliable.

Step-by-Step: A Simple Accrual Month-End Process

- Confirm the cut-off date and closing schedule

- Review open AR and billing cut-off

- Review open AP and bill cut-off

- Identify key accrual categories (payroll, interest, utilities, fees)

- Post accrual journal entries

- Reverse accruals where appropriate (next period)

- Validate reasonableness via flux/variance review

- Lock/report the period and document assumptions

Minimum viable accrual close checklist

Use this when you need a tight process that still holds up in review.

- Confirm the last day of the period and posting rules

- Pull AR aging and look for shipped or delivered but unbilled

- Pull AP detail and look for received but unbilled

- Update payroll accrual based on days earned in period

- Update prepaid amortization schedule

- Update deferred revenue schedule

- Reconcile key accrual accounts to support

- Document assumptions and reviewer sign-off

Accrual Accounting Journal Entries

Common Accrual Journal Entry Examples

Accrual accounting journal entries follow standard debit and credit logic. The goal stays simple. You put the revenue or expense in the right month.

Below are common accrual accounting entries you can copy into your close template.

Accrued expense (utilities):

- Dr Utilities Expense

- Cr Accrued Liabilities (or Utilities Payable)

Accrued wages:

- Dr Wages Expense

- Cr Wages Payable

Accrued revenue (unbilled services):

- Dr Accounts Receivable (or Unbilled Receivable)

- Cr Service Revenue

Deferred revenue (subscription collected upfront):

- At collection:

- Dr Cash

- Cr Deferred Revenue

- Then monthly recognition:

- Dr Deferred Revenue

- Cr Revenue

Prepaid expense amortization:

- Dr Expense

- Cr Prepaid Asset

Tip from practice: name your entries the same way every month.

For example: “ME Accrual – Payroll – Dec 2025.” Review goes faster.

Reversing Entries: When They Help

Reversing entries undo an accrual at the start of the next period. They help when the actual invoice or payroll will hit later and you want to avoid double counting.

However reversing entries can also create noise if no one expects them.

Use them only when the next posting will naturally replace the estimate.

Entry Type → Reverse Next Month? → Why

Revenue Recognition in Accrual Accounting

When Do You Recognize Revenue Under Accrual Accounting?

Revenue recognition accrual accounting records revenue when you satisfy the performance obligation. In plain English, you recognize revenue when you deliver what you promised. You do not wait for the invoice or the payment.

So for accrual revenue recognition, keep three dates separate:

- Delivered or performed (earned)

- Billed (invoiced)

- Paid (cash received)

Only the first one controls revenue timing under accrual accounting.

Common Revenue Recognition Timing Situations

These situations show up in close review across industries.

- Milestone projects (earned vs billed):

You may earn revenue as you hit milestones. Billing may lag or lead. - Monthly subscriptions (ratable recognition):

You recognize revenue evenly across the service period. - Deposits or retainers (often deferred until earned):

You record cash as deferred revenue until you deliver services.

In practice, subscriptions and retainers create the most schedule work.

A clean deferred revenue rollforward prevents errors.

Common Revenue Recognition Mistakes

Most issues come from process gaps, not accounting theory.

Common mistakes:

- Recognizing revenue on invoice date regardless of delivery

- Leaving cash deposits in revenue

- Not tracking unbilled revenue consistently

- Letting “one-off” deals skip the normal review steps

- Not tying revenue support to a clear report or schedule

If you fix the workflow, errors drop fast. You do not need fancy memos.

You need consistent evidence and review.

Why Accrual Accounting Matters for Financial Reporting

What Accrual Accounting Improves

Accrual accounting makes monthly statements more useful. It improves:

- Period comparability

- Visibility into obligations (AP and accrued liabilities)

- Visibility into earned revenue (AR and unbilled)

- Cleaner management reporting and forecasting inputs

It also improves how stakeholders interpret results. Lenders and boards want to see operating reality. Accrual accounting helps you show it.

How Accrual Accounting Impacts Month-End Close

Accrual accounting adds adjustments. More adjustments mean more risk.

Therefore you need a tight close process.

You need:

- Clear ownership for each accrual area

- Standard review steps

- Documentation and consistency

- A sign-off path before you send reports

Common close failure points:

- Late discovery of missing accruals

- Inconsistent treatment client-to-client (for firms)

- Manual review that depends on senior memory

- Accrual accounts that never clear month to month

Practical insight: accruals rarely fail because of math

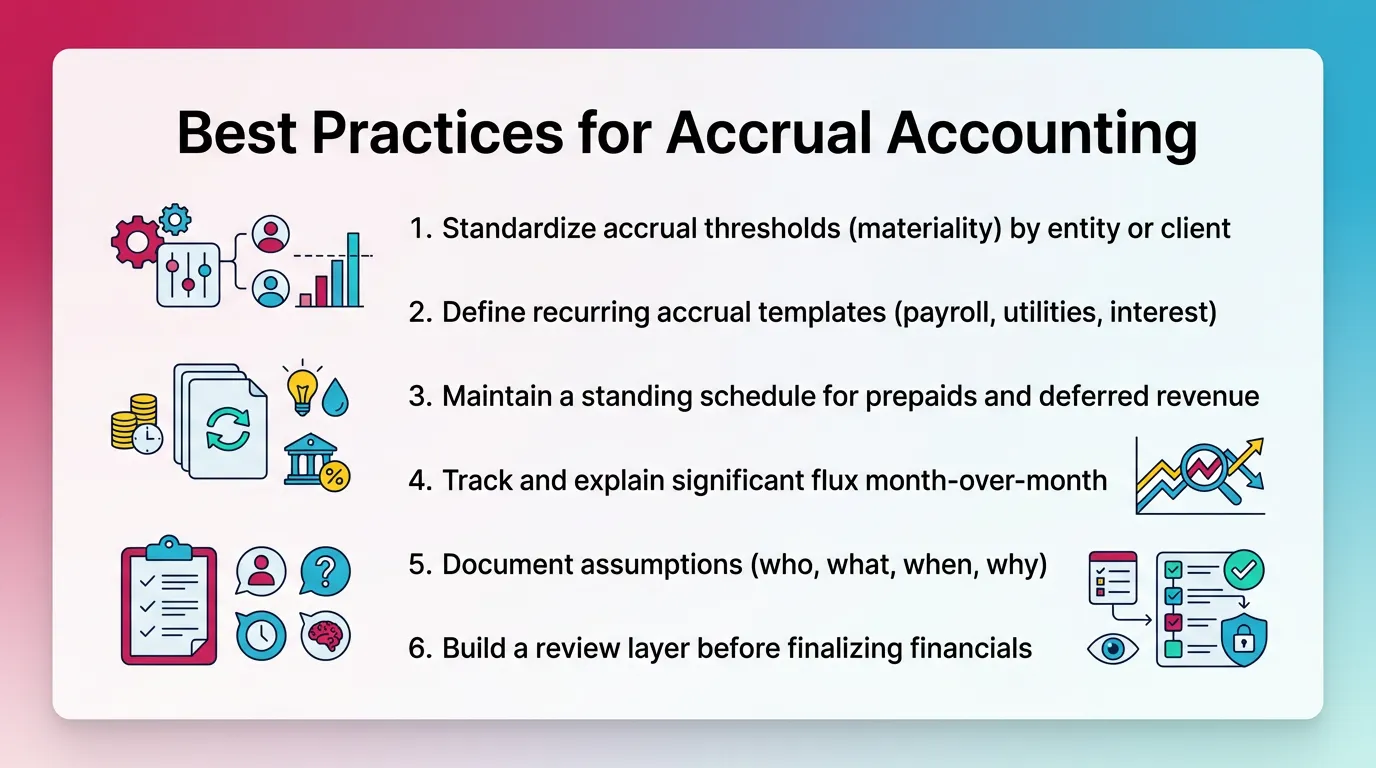

Best Practices for Accrual Accounting

Best Practices Checklist

Accrual accounting works best when you standardize it. Aim for repeatability.

- Standardize accrual thresholds (materiality) by entity or client

- Define recurring accrual templates (payroll, utilities, interest)

- Maintain a standing schedule for prepaids and deferred revenue

- Track and explain significant flux month-over-month

- Document assumptions (who, what, when, why)

- Build a review layer before finalizing financials

One strong habit: do the same reviews in the same order every month.

That reduces rework. It also trains new staff faster.

Common Mistakes to Avoid

These mistakes create messy financials and long closes.

- Accruing without reversing (or reversing without understanding)

- Mixing cash-basis behaviors inside accrual reporting

- Posting accruals without evidence or support

- Ignoring balance sheet rollforward logic (accruals that never clear)

- Not reconciling accrual-related accounts

- Prepaids

- Accrued liabilities

- Deferred revenue

- Unbilled receivables

If an accrual account never clears, treat it as a warning light.

It often signals a process break in AP, billing, or payroll.

How Xenett Supports Consistent Accrual Review During Month-End Close

Xenett helps teams run a consistent close. It supports accrual review, task flow, and sign-off. It does not replace accounting judgment. It also does not perform audits or provide audit services.

Turning Accrual Best Practices Into a Repeatable Close System

Accruals look simple on paper. Operations make them drift.

Teams post entries late. Support sits in folders. Reviews vary by reviewer.

Xenett helps by making review-first work visible. Account findings drive tasks.

Therefore the team works from the same source of truth each close.

Close Task and Checklist Management

Xenett lets you convert recurring accrual work into repeatable checklists.

For example, you can standardize:

- Payroll accrual steps and inputs

- AP cut-off review steps

- Unbilled revenue review steps

- Prepaid and deferred revenue schedule updates

You also control sequence. Cut-off comes before entries. Review comes before final. This reduces “tribal knowledge” across staff.

Related Xenett resource on close workflow management:

https://www.xenett.com/

Review and Approval Workflows

Accrual areas need structured review. Otherwise late changes slip in.

With Xenett, teams can route work for review in a consistent way, such as:

- AR and billing cut-off

- AP cut-off and accruals

- Deferred revenue and revenue recognition schedules

- Accrued liabilities rollforward checks

You can record approvals and handoffs. This prevents last-minute edits after review. It also protects the integrity of the reporting package.

Visibility Into Close Status and Bottlenecks

Accrual close work fails when blockers stay hidden.

Xenett gives visibility into:

- What is complete

- What is pending

- What is blocked on support or responses

This helps you spot patterns. For example, you may always wait on invoices from one vendor. You can then fix the upstream process.

FAQ: Accrual Accounting

What Is Accrual Accounting in Simple Terms?

Accrual accounting records revenue when earned and expenses when incurred, even if cash has not moved yet. It focuses on when business activity happens.

What Is an Accrual in Accounting?

An accrual is an entry used to record revenue or expenses in the correct period before cash is received or paid. It fixes timing at period-end.

What Is the Best Example of Accrual Accounting?

A sale made in December and paid in January gets recorded as December revenue under accrual accounting. Cash collection does not control the revenue date.

What Are the Main Types of Accruals?

The main types include accrued expenses, accrued revenue, prepaid expenses, and deferred revenue. These categories cover most month-end timing issues.

What Is the Difference Between Cash and Accrual Accounting?

Cash basis records transactions when money changes hands. Accrual basis records when the activity happens, meaning when you earn revenue or incur expenses.

Why Is Accrual Accounting Used in Financial Reporting?

It provides a more accurate view of profitability and obligations for a specific period. It also improves comparability across months.

What Are Common Accrual Accounting Journal Entries?

Common entries include accrued wages, utilities payable, unbilled revenue or AR, deferred revenue recognition, and prepaid expense amortization. These entries align timing to the month.

How Does Accrual Accounting Affect Month-End Close?

It adds required timing adjustments and increases the need for consistent review, documentation, and sign-off before reports are finalized. It also increases the need to reconcile accrual accounts.

Conclusion

Accrual accounting gives you a cleaner view of performance and obligations. It also makes month-end close more structured. You need cut-off discipline, repeatable entries, and consistent review.

If you want to tighten your accrual close, start with one change. Standardize your accrual checklist and your review steps. Then document assumptions the same way each month.

Use Xenett to operationalize that process with clear tasks, routing, and sign-off. Keep judgment with your team. Make execution consistent.