.webp)

.svg)

Revenue Recognition: Complete Guide with Examples

.jpg)

Blog Summary / Key Takeaways

- Revenue recognition records revenue when you deliver value, not when you bill.

- ASC 606 uses a 5-step revenue recognition process built on control transfer.

- Deferred revenue and contract assets should reconcile every month.

- Journal entries stay simple, but edge cases need strong documentation.

- Close success depends on repeatable workflows and visible review.

What Is Revenue Recognition in Accounting?

Revenue Recognition

Revenue recognition is the accounting process of recording revenue in the period it is earned, not necessarily when cash is received.

That means you tie revenue to delivery. You do not tie it to invoices.

Revenue Recognition vs Cash Collection (Common Confusion)

Cash timing and revenue timing often diverge under accrual accounting. That gap creates the accounts your team reconciles every month.

Here is where you usually see the difference:

- Deferred revenue (contract liability). You billed or got paid first.

- Accrued revenue (contract asset / unbilled). You earned it first.

- Contract assets and liabilities. These track timing, not cash.

A practical example:

- You bill $120,000 upfront for a 12-month SaaS term.

- Cash hits today. Revenue posts monthly.

- The balance sits in deferred revenue until earned.

When to Recognize Revenue

Recognize revenue when control transfers and the performance obligation is satisfied. You either recognize at a point in time or over time.

Common patterns:

- Point in time. Delivery, installation acceptance, or title transfer.

- Over time. Continuous service or progress toward completion.

Control does the heavy lifting under ASC 606. If you can show control moved, you can support revenue timing.

What Is the Revenue Recognition Principle?

The Revenue Recognition Principle in Accounting (GAAP Concept)

The revenue recognition principle says you recognize revenue when it is earned and realized or realizable. ASC 606 modernizes this and centers it on transfer of control.

If you ask, “what is the revenue recognition principle in accounting,” the best short answer stays the same. Record revenue when you deliver what you promised.

Why Is Revenue Recognition Important? (For Finance Leaders + Accountants)

Revenue timing drives the story your financials tell. It also drives audit risk.

Revenue recognition impacts:

- Gross margin trends and EBITDA patterns.

- Forecast credibility and board reporting.

- Compliance under revenue recognition standards.

- Audit readiness and restatement risk.

A real close insight from practice:

Most revenue issues start as “small deal exceptions.” They end as big close surprises.

One late contract change can break the deferred revenue roll-forward.

Therefore, teams win when they systematize revenue recognition accounting.

Revenue Recognition Standards: ASC 606 vs IFRS 15 (What’s the Difference?)

What Is 606 Revenue Recognition?

ASC 606 is the US GAAP standard for revenue from contracts with customers. People also call it “606 revenue recognition.”

ASC 606 aims to make revenue more comparable across industries. It does that through one core model and stronger disclosures.

ASC 606 vs IFRS 15

Both standards align closely. However, differences still show up in practice.

They show up in wording, practical expedients, and disclosure expectations.

ASC 606 vs IFRS 15

Revenue Recognition Disclosures (Often Underestimated)

Disclosures take time. They also require clean roll-forwards.

Common disclosure areas:

- Contract balances. Deferred revenue and contract assets.

- Changes in contract balances. Opening to closing.

- Remaining performance obligations (RPO).

- Significant judgments. Variable consideration and timing.

If your schedules do not tie out monthly, disclosures become painful.

That pain hits at quarter-end and year-end first.Revenue Recognition Steps During Month-End Close

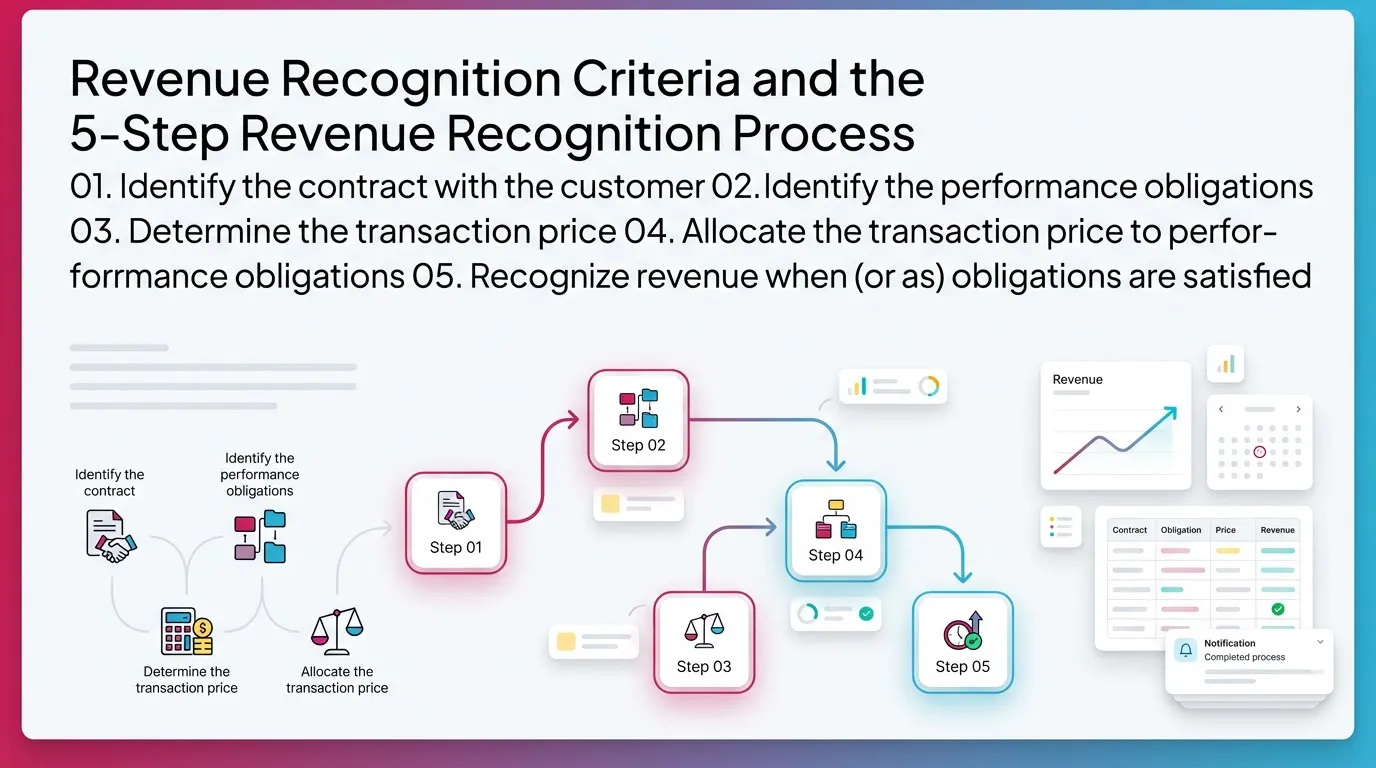

Revenue Recognition Criteria and the 5-Step Revenue Recognition Process (ASC 606 / IFRS 15)

The 5 Steps of Revenue Recognition

- Identify the contract with the customer

- Identify the performance obligations

- Determine the transaction price

- Allocate the transaction price to performance obligations

- Recognize revenue when (or as) obligations are satisfied

These revenue recognition steps sound simple. They get complex in edge cases.

Step 1: Identify the Contract

A contract exists when specific revenue recognition criteria are met.

You need enforceable rights and obligations.

Check these items:

- Both parties approved and committed.

- Rights are identifiable.

- Payment terms are identifiable.

- The contract has commercial substance.

- Collectability is probable.

If collectability fails, stop. You may have cash receipts but no contract.

That changes presentation and disclosures.

Step 2: Identify Performance Obligations

Performance obligations are promises to transfer goods or services.

You account for them if they are “distinct.”

A good shortcut:

- Can the customer benefit from it on its own or with other resources?

- Is it separately identifiable from other promises?

Common bundling pitfalls:

- Onboarding + subscription.

- Support + license.

- Implementation + managed services.

In SaaS revenue recognition, implementation drives many disputes.

Some teams treat all setup fees the same. That causes inconsistency.

Step 3: Determine the Transaction Price

Transaction price equals what you expect to receive.

However, it rarely equals the invoice total in modern deals.

Common adjustments:

- Variable consideration. Usage, rebates, credits, penalties.

- Constraint. Include variable amounts only if reversal is unlikely.

- Financing components. Timing value of money in some cases.

- Non-cash consideration. Equity, barter, or credits.

- Consideration payable to customer. Credits or co-marketing.

This is where many revenue recognition accounting memos start.

Your documentation needs to show your judgment and your math.

Step 4: Allocate the Transaction Price

Allocate price to performance obligations based on SSP.

SSP means standalone selling price.

Common SSP methods:

- Adjusted market assessment approach.

- Expected cost plus a margin approach.

- Residual approach (only when permitted).

Example allocation situation:

You sell a subscription with implementation and premium support.

You need SSPs for each element. Then allocate the discount.

If SSPs drift over time, your allocation drifts too.

Therefore, you need an SSP refresh cadence and governance.

Step 5: Recognize Revenue

Recognize revenue when you satisfy the obligation.

That can happen at a point in time or over time.

Over-time recognition usually fits when:

- The customer receives benefits as you perform.

- You create or enhance an asset the customer controls.

- You have no alternative use and you have enforceable payment rights.

Methods to measure progress:

- Output methods. Milestones, units delivered, surveys of work.

- Input methods. Cost-to-cost, labor hours, machine hours.

Acceptance clauses matter. So does delivery evidence.

If legal terms say “no acceptance, no delivery,” your timing shifts.

Revenue Recognition Methods

Common Revenue Recognition Methods

Revenue recognition methods describe how you measure and time revenue.

They must still align to the ASC 606 model.

Common methods:

- Point-in-time. Hardware delivery or a software license key.

- Straight-line / ratable. SaaS subscriptions and support.

- Percentage of completion. Long projects with over-time criteria.

- Milestone method. If milestones reflect performance.

- Usage-based recognition. Consumption pricing or transaction fees.

Teams often misuse “straight-line” as a default.

However, you must first confirm the obligation is a stand-ready service.

Method Selection: Decision Tree

Use these prompts to choose point-in-time vs over-time recognition.

Answer in order.

- Is the customer receiving benefits as you perform?

- Is there an alternative use for the asset you create?

- Is payment enforceable for performance completed to date?

If you answer “yes” to the over-time criteria, measure progress.

If you answer “no,” look for the point-in-time transfer indicators.

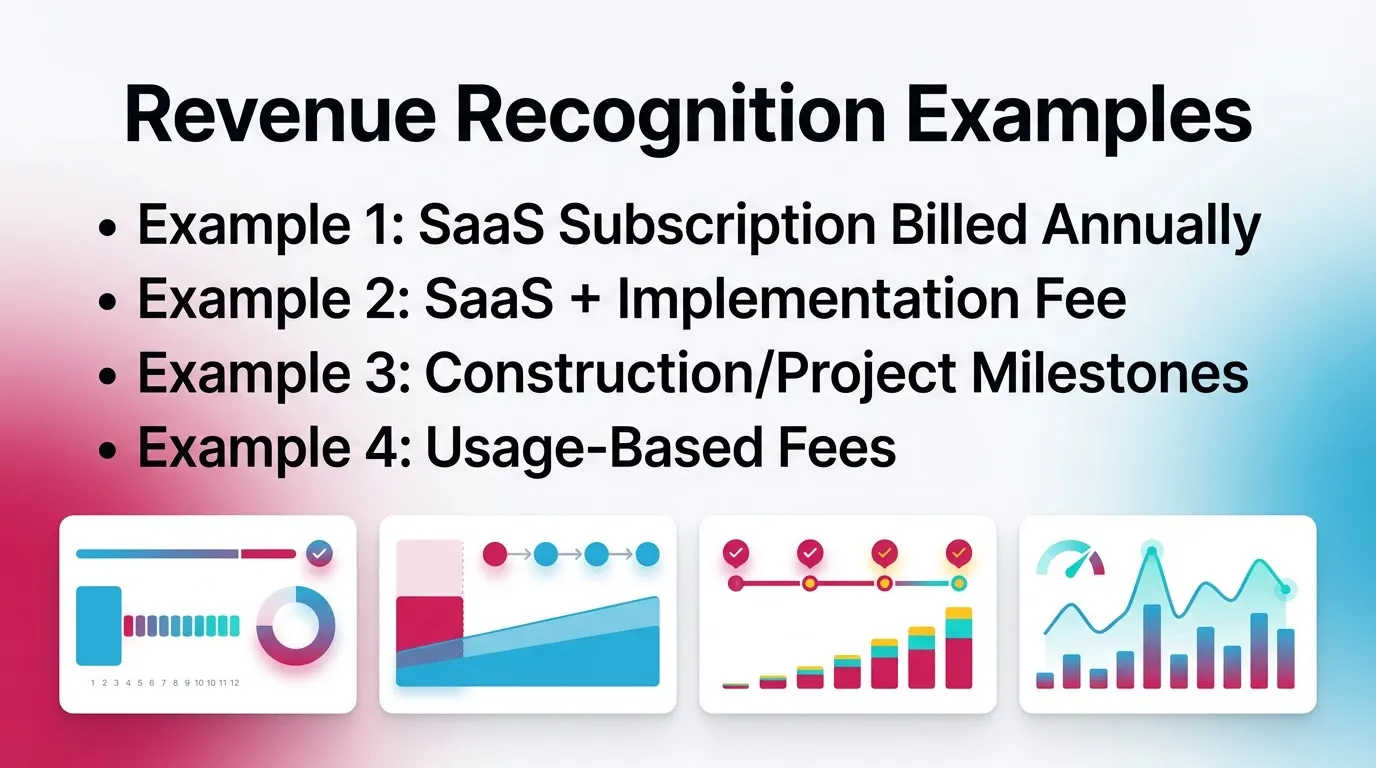

Revenue Recognition Examples

Example 1: SaaS Subscription Billed Annually (Deferred Revenue → Ratable Revenue)

You bill $12,000 on January 1 for a 12-month term. Cash comes in.

You recognize revenue monthly at $1,000.

Close impact: you must tie out deferred revenue every month.

You need an opening balance, billings, revenue recognized, and closing.

A clean roll-forward catches issues fast. For example:

- A credit memo posted to revenue instead of deferred revenue.

- A backdated contract start date.

Example 2: SaaS + Implementation Fee (Bundled Arrangement)

You sell:

- 12-month subscription: $24,000

- Implementation: $6,000

Total invoice: $30,000

First question: are obligations distinct?

- Subscription usually is distinct.

- Implementation depends on facts and the promise.

If implementation is distinct, allocate using SSP.

Then recognize:

- Subscription ratably over 12 months.

- Implementation at point in time or over time.

If implementation is not distinct, combine it with the subscription.

Then recognize the combined obligation over the subscription term.

This is the SaaS revenue recognition issue I see most.

Sales calls it “setup.” Accounting needs to map the promise.

Example 3: Construction/Project Milestones

You build a custom asset on the customer’s site.

The customer controls the work in progress. That supports over-time.

Two ways to recognize revenue:

- Percentage of completion using cost-to-cost.

- Milestones if they match performance.

Evidence you need:

- Approved budgets and forecasts.

- Progress reports.

- Change orders and scope tracking.

Change orders break schedules fast. Track them weekly, not monthly.

Example 4: Usage-Based Fees

You charge $0.05 per API call.

You recognize revenue as usage occurs.

If the contract includes minimums, reassess variable consideration.

Apply the constraint when reversal risk exists.

Revenue Recognition Examples by Contract Type

Revenue Recognition Journal Entries

Core Journal Entries You’ll Use Most Often

These revenue recognition journal entries cover most closes.

They also drive most tie-outs.

Invoice issued before performance:

- Dr Accounts Receivable

- Cr Deferred Revenue (Contract Liability)

Revenue recognized over time:

- Dr Deferred Revenue

- Cr Revenue

Accrued revenue (earned not billed):

- Dr Contract Asset (or Unbilled A/R)

- Cr Revenue

Tip from the field:

If your team posts revenue straight from invoices, stop and reset.

Billing schedules rarely equal revenue schedules under ASC 606.

Journal Entries for Common Edge Cases

Edge cases create true-ups and audit questions.

Document them as you post them.

Common cases:

- Contract modifications. Prospective or cumulative catch-up.

- Refund liabilities. Expected credits and returns.

- Write-offs. Separate bad debt policy from revenue policy.

Write-offs usually hit allowance and bad debt.

Do not “reverse revenue” unless guidance requires it.

Revenue Recognition Journal Entries Cheat Sheet

Revenue Recognition Accounting: The Operational Process (Who Does What During Close?)

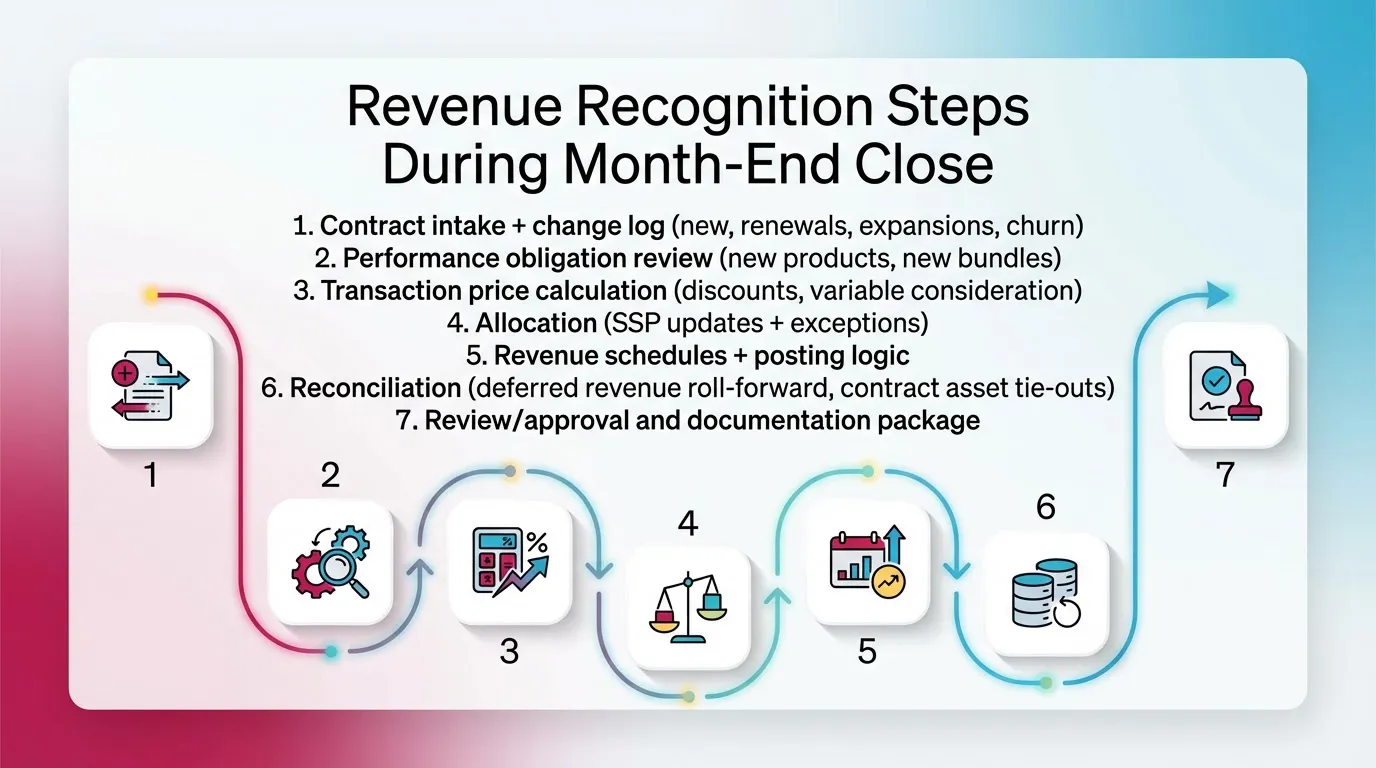

Revenue Recognition Steps During Month-End Close (Practical Workflow)

Revenue recognition accounting works best as a repeatable close stream.

You need clear inputs, owners, and review points.

A practical month-end workflow:

- Contract intake + change log (new, renewals, expansions, churn)

- Performance obligation review (new products, new bundles)

- Transaction price calculation (discounts, variable consideration)

- Allocation (SSP updates + exceptions)

- Revenue schedules + posting logic

- Reconciliation (deferred revenue roll-forward, contract asset tie-outs)

- Review/approval and documentation package

In practice, steps 1 and 6 cause most delays.

Teams miss changes. Then tie-outs fail at the end.

Controls and Evidence Checklist

You do not need fancy controls. You need consistent ones.

Make them easy to execute every month.

Evidence checklist:

- Version-controlled contract repository.

- Approval trail for key judgments.

- SSP policy and refresh record.

- Variable consideration support and constraint logic.

- Reconciliation workpapers and roll-forwards.

I have watched strong teams cut close time by days with one change.

They forced every non-standard deal into a short revenue memo.

That memo prevented rework later.

How to Audit Revenue Recognition

Finance teams ask “how to audit revenue recognition” for one reason.

They want fewer audit questions and faster fieldwork.

This section focuses on audit prep, not audit procedures.

What Auditors Typically Test

Auditors test what tends to break or move results.

Revenue remains a presumed fraud risk in many audits.

Common focus areas:

- Contract identification and completeness.

- Cutoff around period end.

- Variable consideration and constraints.

- SSP allocation methodology.

- Contract modifications and concessions.

Auditors also test IT reports that feed revenue schedules.

If you use system exports, keep report logic consistent.

Revenue Recognition Audit Prep Checklist

Prep these items before auditors ask. It saves real time.

Checklist:

- Contract population completeness tie-out.

- Deferred revenue roll-forward support.

- Revenue schedules by material product line.

- Evidence for over-time recognition (progress reports).

- Management review documentation and sign-offs.

Do not wait for PBC lists to start this work.

Build it into your month-end close package.

Best Practices for Revenue Recognition

Best Practices That Scale (Especially for SaaS Revenue Recognition)

You stay compliant by reducing variation and tightening review.

That matters most in SaaS revenue recognition.

Best practices that scale:

- Standardize contract language to reduce edge cases.

- Maintain an SSP policy and refresh cadence.

- Require a revenue memo threshold for non-standard deals.

- Automate roll-forwards and reconcile monthly.

- Separate calculation from review to avoid self-approval.

- Build a revenue close calendar with dependencies.

A practical cadence that works:

- Weekly contract change review with Sales Ops.

- Monthly SSP exception review.

- Quarterly disclosure readiness check.

Common Mistakes (And How They Show Up in the Close)

Mistakes show up as tie-out breaks. Or they show up as late JEs.

Common issues:

- Treating billing schedules as revenue schedules.

- Missing contract modifications and concessions.

- Ignoring variable consideration constraints.

- Inconsistent treatment of setup fees.

- Weak cutoff around period end.

Best Practices vs Common Mistakes

How Xenett Helps Teams Operationalize Revenue Recognition Controls During Close

Xenett helps teams execute revenue work the same way every month.

It improves visibility, review, and close discipline.

Xenett is not an audit tool. Xenett does not provide audit services.

It supports accounting workflow and close management only.

Close Task and Checklist Management

Revenue work fails when it lives in tribal knowledge.

A checklist makes it repeatable.

With Xenett, teams can standardize tasks for:

- Deferred revenue roll-forward and tie-out.

- Revenue schedule review and variance checks.

- Contract change review and exception logging.

- Cutoff checks and support retention.

You can also set dependencies.

For example, you can block “Finalize revenue” until roll-forwards tie.

Review and Approval Workflows

Revenue recognition process decisions need visible review.

That includes SSP changes and unusual allocations.

Xenett helps teams:

- Route revenue close items to the right reviewer.

- Capture reviewer notes next to the task evidence.

- Keep decisions out of Slack threads and inbox searches.

This matters when staff turns over.

It also matters when auditors ask “who approved this judgment.”

Visibility Into Close Status and Bottlenecks

Revenue is rarely one account. It is a system of schedules.

Visibility helps you manage the system.

Xenett gives controllers and firm leads a live view of:

- What is done and what is pending.

- Where close gets stuck each month.

- Which entities lag on revenue tie-outs.

Therefore, you fix root causes instead of chasing symptoms.

Revenue Recognition Software: When Spreadsheets Stop Working

Signs You Need Revenue Recognition Software

Spreadsheets work early. Then contract volume grows.

Then modifications explode. Then spreadsheets break.

Common signs:

- Many contract variations and modifications.

- Manual SSP allocation and fragile formulas.

- Deferred revenue does not reconcile cleanly.

- Close delays caused by revenue tie-outs.

- Audit requests require days of rebuild work.

If you see these, consider revenue recognition software.

Keep your close workflow tool separate from your rev rec engine.

Revenue Recognition Software Evaluation Checklist

Use this checklist to evaluate tools without vendor bias.

Focus on controls, audit trail, and schedule integrity.

Checklist:

- ASC 606/IFRS 15 support for the 5-step model.

- Contract modification handling.

- SSP management and allocation audit trail.

- Automated posting and clear reconciliation outputs.

- Reporting for roll-forwards and waterfalls.

- Controls for approvals, change logs, and evidence retention.

Spreadsheet vs Revenue Recognition Software

FAQ

What is revenue recognition?

Revenue recognition is the accounting practice of recording revenue when it’s earned by satisfying performance obligations, not simply when cash is received.

What is the revenue recognition principle?

The revenue recognition principle requires revenue to be recognized when it is earned and realizable. Under ASC 606, it aligns to transfer of control to the customer.

What are the 5 steps of revenue recognition under ASC 606?

The revenue recognition steps are: identify the contract, identify performance obligations, determine the transaction price, allocate the price, and recognize revenue when (or as) obligations are satisfied.

When should revenue be recognized?

Recognize revenue when control transfers to the customer and the performance obligation is satisfied. Recognize at a point in time or over time based on the facts.

What are common revenue recognition methods?

Common revenue recognition methods include point-in-time, ratable (straight-line), percentage-of-completion, milestone-based, and usage-based recognition.

What are revenue recognition criteria?

Revenue recognition criteria include an enforceable contract, identifiable rights and payment terms, commercial substance, probable collectability, and satisfaction of performance obligations.

What is deferred revenue in revenue recognition?

Deferred revenue is a contract liability recorded when a customer pays or is billed before you deliver the related goods or services.

What are typical revenue recognition journal entries?

Typical revenue recognition journal entries include: debit A/R and credit deferred revenue when invoicing early, then debit deferred revenue and credit revenue as you perform.

How do you audit revenue recognition?

Auditors typically focus on contract completeness, cutoff, performance obligations, variable consideration, SSP allocation, modifications, and reconciliation of contract balances. Finance teams can prep roll-forwards and review support.

What is SaaS revenue recognition?

SaaS revenue recognition usually posts revenue ratably over the subscription term. It also requires careful treatment of implementation fees, usage charges, and bundled arrangements.

Conclusion

Revenue recognition works best when you treat it like a close process, not a one-time policy. Document judgments early. Reconcile contract balances monthly. Review exceptions every close.

If your team wants fewer surprises, start by turning your revenue recognition steps into a repeatable checklist. Then assign owners, due dates, and reviews. That is the fastest path to steady compliance.