.svg)

What Is Account Reconciliation and How Does It Work

.jpg)

Ask questions, get summaries, or uncover key takeaways from this article.

.webp)

Summary / Key Takeaways

- Account reconciliation compares two sets of records to confirm they match and are accurate

- It covers bank accounts, credit cards, balance sheet accounts, intercompany accounts, and more

- Most firms reconcile at month end as part of the financial close process

- Skipping reconciliation means errors compound silently until they become expensive to fix

- Xenett's Close Dashboard gives firms real-time visibility into reconciliation status across all clients

Most accounting errors are not dramatic.

They do not show up as obvious fraud or a missing payment.

They show up as a $47 difference in a bank account that nobody followed up on. Then it is $214 next month because no one caught the first one. Then it is a problem at year end that takes three hours to untangle.

Account reconciliation is the process that prevents that. It is also one of the most delayed and manual parts of the accounting workflow at most firms.

This guide explains what account reconciliation is, how it works, which types your firm should be running, and what a clean reconciliation process actually looks like.

What Is Account Reconciliation?

Account reconciliation is the process of comparing two sets of financial records to verify they are consistent, accurate, and complete.

In practice, that usually means comparing your internal ledger balance to an external statement, a bank statement, a credit card statement, a vendor invoice, or a sub-ledger and explaining any differences.

If the two records match, the account is reconciled. If they do not, you find out why, fix the underlying issue, and document the resolution.

That is the whole process. The complexity comes from doing it at scale, across dozens of accounts and clients, on a deadline.

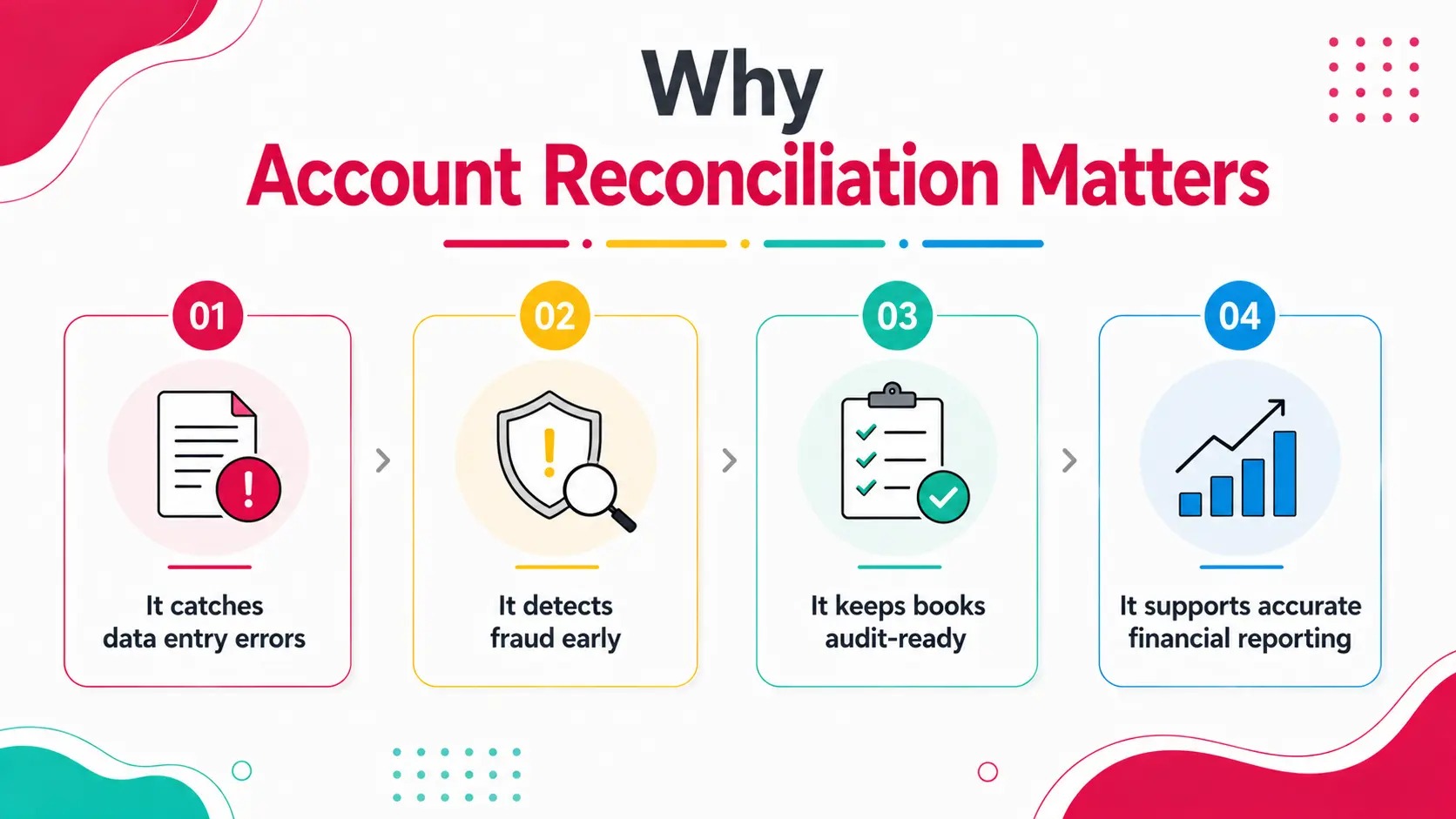

Why Account Reconciliation Matters

Reconciliation is not a compliance checkbox. It is the primary mechanism for catching errors before they become material problems.

It catches data entry errors. Duplicate transactions, transposed numbers, and miscategorized expenses all show up during reconciliation. Catch them in month one and they take five minutes to fix. Miss them for six months and the correction becomes a project.

It detects fraud early. Unauthorized transactions, ghost vendors, and duplicate payments are most visible when account activity is reviewed systematically. Firms that reconcile regularly catch these patterns early.

It keeps books audit-ready. If your clients' books are reconciled monthly, year end is a review, not a reconstruction. If reconciliation has been skipped, year end becomes a weeks-long cleanup exercise.

It supports accurate financial reporting. A P&L built on unreconciled accounts is an estimate. Management decisions and tax filings made from unreconciled books carry real risk.

Types of Account Reconciliation

Not all reconciliations are the same. Here are the main types accounting firms handle regularly.

Bank reconciliation is the most familiar. But for a clean close, balance sheet reconciliation reconciling every balance sheet account, not just cash is the standard that well-run firms hold themselves to.

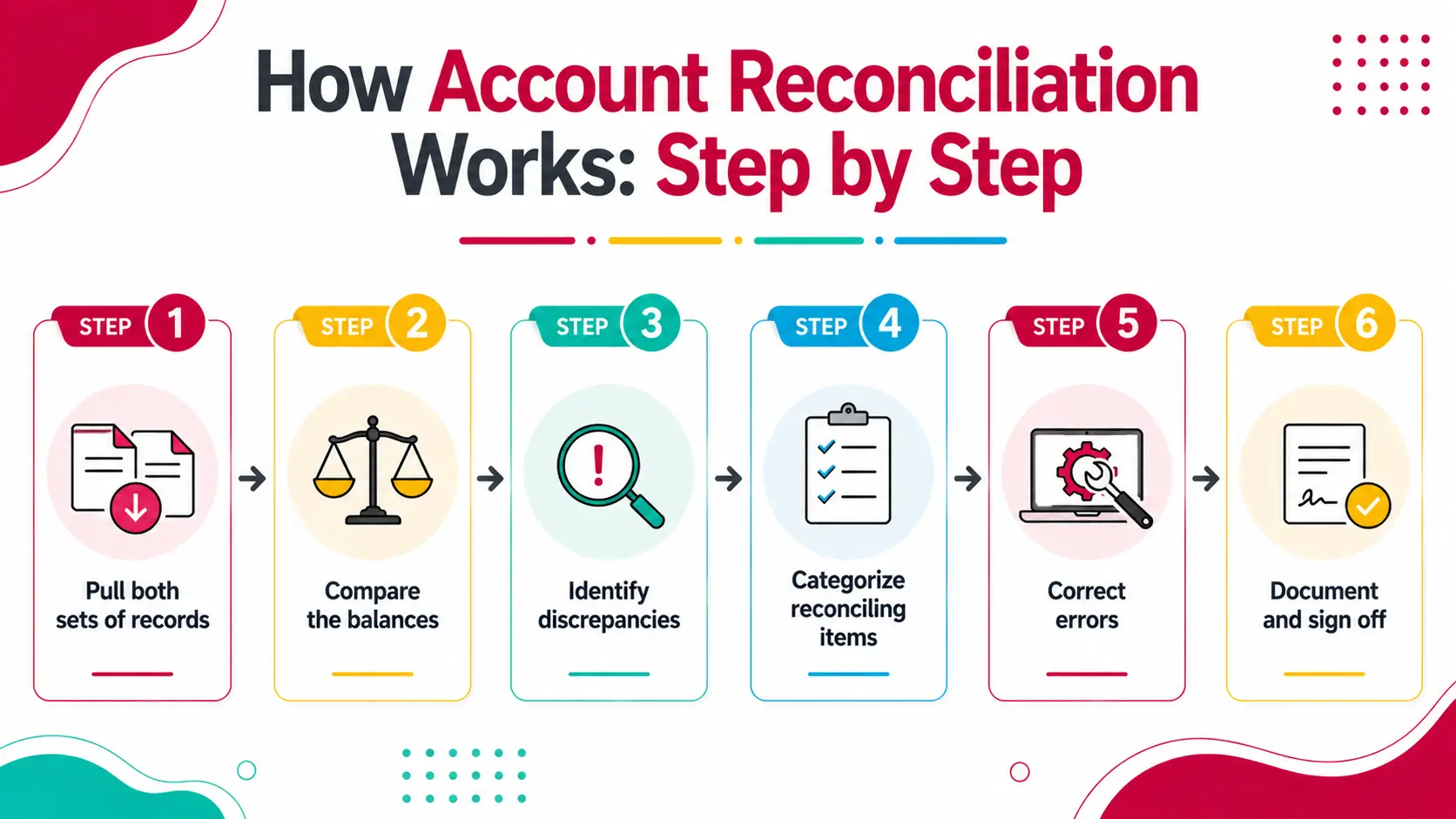

How Account Reconciliation Works: Step by Step

The process is consistent across account types. The source documents change.

Step 1: Pull both sets of records. Get the GL balance for the account as of the reconciliation date. Get the external statement or supporting document for the same period.

Step 2: Compare the balances. If they match, the account is reconciled. Document it and move on.

Step 3: Identify discrepancies. If they do not match, list every item in one record that does not appear in the other. These are your reconciling items.

Step 4: Categorize reconciling items. Some discrepancies are timing differences transactions recorded in the GL but not yet cleared at the bank. These are expected. Others are errors: duplicate entries, missing transactions, wrong amounts. These need to be corrected.

Step 5: Correct errors. Post adjusting journal entries for any errors. Timing differences are noted and explained but not corrected they will clear in the next period.

Step 6: Document and sign off. Record the reconciliation with opening balance, activity, reconciling items, ending balance, and who prepared and reviewed it. This is your audit trail.

Balance Sheet Reconciliation vs. Bank Reconciliation

These two are often confused. They are related but different in scope.

Bank reconciliation is a subset of balance sheet reconciliation. Firms that only reconcile cash are leaving significant risk unmanaged across the rest of the balance sheet.

Where Most Firms Get Reconciliation Wrong

After working with 1,000+ accounting firms, these are the failure patterns that show up most consistently.

Reconciling once at year end instead of monthly. By the time year end arrives, 12 months of unresolved discrepancies have compounded. What would have been a 10-minute fix in January is a multi-hour investigation in December.

No standard format for reconciliation documentation. If every preparer documents reconciliations differently or does not document them at all the review process breaks down. Reviewers cannot verify work they cannot read.

No visibility into status across clients. At a firm managing 30 or 40 bookkeeping clients, there is no easy way to know which accounts are reconciled, which are in progress, and which have outstanding items unless a system is tracking that.

Review happening over email. Reconciliation workpapers sent as attachments, reviewed in email, corrections communicated back in a thread. This is the default at most firms. It is slow, error-prone, and leaves no clean audit trail.

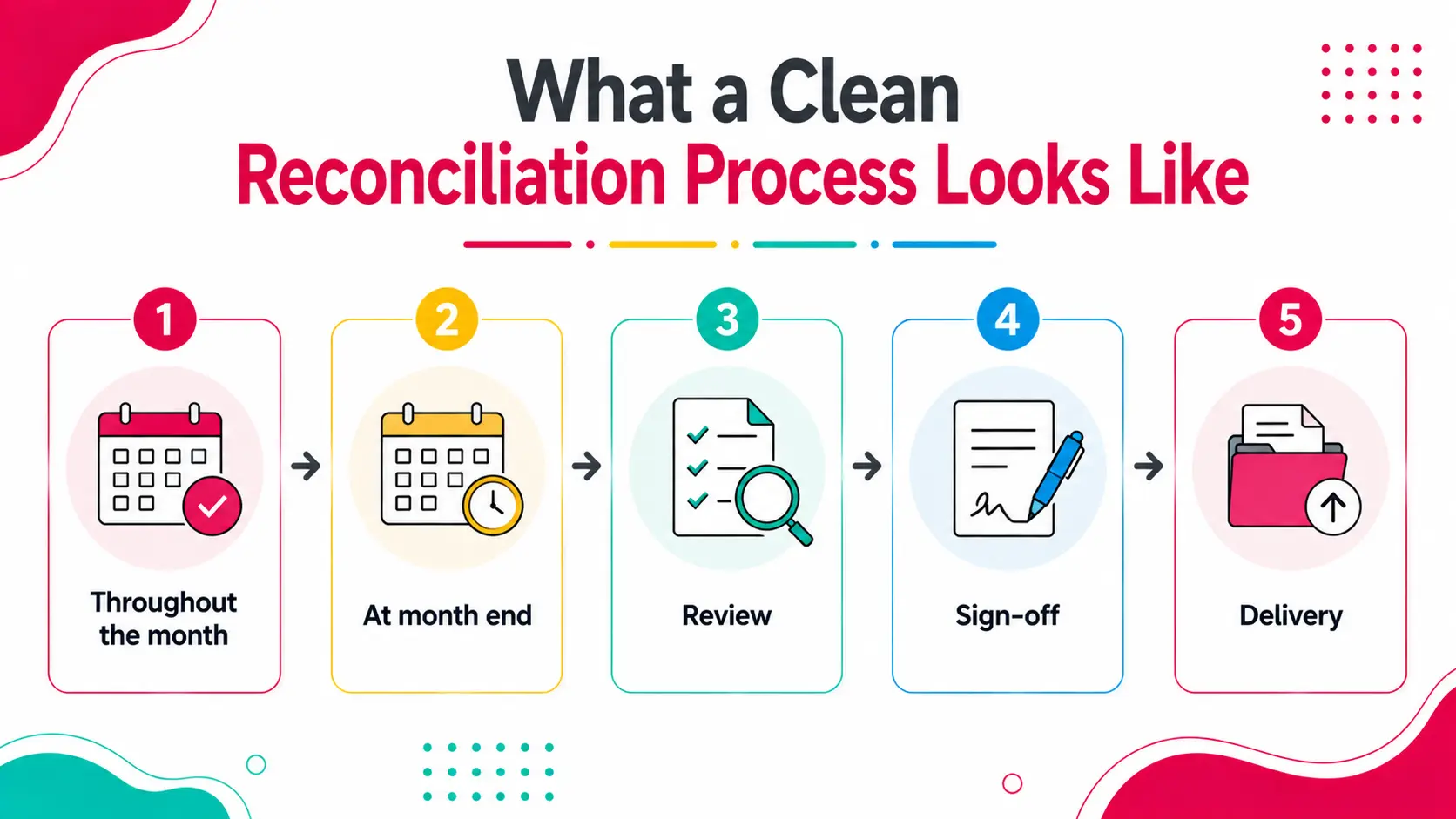

What a Clean Reconciliation Process Looks Like

Here is what a structured reconciliation workflow looks like at a firm managing multiple bookkeeping clients.

Throughout the month: The bookkeeper categorizes transactions, follows up on uncategorized items, and flags anything unusual as it appears. Reconciliation is faster when the books are kept current.

At month end: The bookkeeper pulls the bank statement, runs the reconciliation in QBO or Xero, resolves all outstanding items, and marks the account reconciled. For balance sheet accounts, supporting schedules are updated and tied to GL balances.

Review: The completed reconciliation with all supporting documentation moves to the reviewer through the practice management workflow. The reviewer checks for unresolved items, reviews the reconciling item list, and approves or sends back with specific comments. No email.

Sign-off: The partner or manager approves. The reconciliation is documented with preparer, reviewer, and date. The client account status updates automatically.

Delivery: Reconciled financials go to the client. Any issues found during reconciliation that need client attention are flagged directly.

Real Scenario: A $14,000 Error That Built for 4 Months

A seven-person bookkeeping firm took on a restaurant client mid-year. The prior bookkeeper had not reconciled the sales tax liability account in four months.

During the first month-end close, the bookkeeper noticed the sales tax liability balance did not match the tax filing records. After tracing back four months of transactions, the error was clear: a $3,500 monthly sales tax payment had been recorded as an expense rather than a liability reduction. Four months of that error totaled $14,000 in misstated financials.

The client had filed a quarterly tax return based on those numbers. A correction and amended filing were required.

The prior bookkeeper was not careless. They simply were not reconciling liability accounts - only cash. Everything looked fine on the surface. Bank reconciled. Books balanced. But the balance sheet was wrong.

Monthly balance sheet reconciliation would have caught this in month one.

How Xenett Can Help

Xenett's Close Dashboard is built around the reconciliation and close workflow. It gives firms real-time visibility into where every client account stands - what is reconciled, what is in review, what has open items, and what is waiting on client information.

Key capabilities:

- Close Dashboard - Firm-level view of close status across all clients. See which accounts are reconciled, in progress, or blocked in one screen.

- Structured review workflows - Reconciliation workpapers move from preparer to reviewer to partner with comments tied to the work item. No email chains.

- Status tracking - Every reconciliation has a status: not started, in progress, in review, approved.

- Document management - Supporting schedules and reconciliation documentation stored and versioned in one place.

- Recurring task automation - Monthly reconciliation tasks auto-generate for every client on schedule.

Firms using Xenett report 70% less review time and 3x faster close cycles.

Book a 15-minute demo to see the Close Dashboard in action.

FAQs

What is the purpose of account reconciliation?

Account reconciliation verifies that two sets of records are consistent and accurate. It catches errors, identifies fraud, ensures the books reflect reality, and keeps financial statements reliable. It is the primary quality control step in the monthly close process.

How often should accounts be reconciled?

Most accounts should be reconciled monthly especially cash, credit cards, accounts receivable, and accounts payable. Fixed assets and prepaid schedules may be reconciled quarterly. The higher the activity in an account, the more frequently it needs reconciliation.

What is the difference between bank reconciliation and account reconciliation?

Bank reconciliation is one type of account reconciliation. It compares the GL cash balance to the bank statement. Account reconciliation is broader and covers every balance sheet account, each compared to its own supporting documentation.

What are common reconciling items?

Common reconciling items include outstanding checks not yet cleared at the bank, deposits in transit, bank fees not yet recorded in the GL, timing differences on automatic payments, and data entry errors. Most are timing differences. Actual errors need to be corrected with journal entries.

What happens if accounts are not reconciled?

Errors accumulate and compound. Small discrepancies become larger ones. By year end, the cleanup is significantly more time-consuming than monthly reconciliation would have been. In the worst case, financial statements are materially misstated, tax filings are incorrect, and clients face penalties.

Who is responsible for account reconciliation in an accounting firm?

Typically the bookkeeper or staff accountant prepares the reconciliation and a manager or partner reviews and approves it. The two-stage review -- preparer and reviewer -- is standard practice for maintaining accuracy and accountability.

How does account reconciliation work in QuickBooks?

In QuickBooks Online, you run the reconciliation from the Banking menu. You select the account, enter the statement ending balance, and mark off cleared transactions. QBO calculates the difference. When the difference is zero, the account is reconciled and QBO records the reconciliation date and balance.

Conclusion

Account reconciliation is one of the most routine tasks in accounting.

It is also one of the most important. Clean reconciliations mean clean books. Clean books mean accurate financial statements. Accurate financial statements mean clients can make decisions, file taxes, and plan with confidence.

The firms that do this well - monthly, systematically, with a structured review process, spend less time on year-end cleanup, catch problems before they compound, and deliver work clients can trust.

See how Xenett's Close Dashboard supports a clean reconciliation workflow.

Account reconciliation verifies that two sets of records are consistent and accurate. It catches errors, identifies fraud, ensures the books reflect reality, and keeps financial statements reliable. It is the primary quality control step in the monthly close process.

Most accounts should be reconciled monthly especially cash, credit cards, accounts receivable, and accounts payable. Fixed assets and prepaid schedules may be reconciled quarterly. The higher the activity in an account, the more frequently it needs reconciliation.

Bank reconciliation is one type of account reconciliation. It compares the GL cash balance to the bank statement. Account reconciliation is broader and covers every balance sheet account, each compared to its own supporting documentation.

Common reconciling items include outstanding checks not yet cleared at the bank, deposits in transit, bank fees not yet recorded in the GL, timing differences on automatic payments, and data entry errors. Most are timing differences. Actual errors need to be corrected with journal entries.

Errors accumulate and compound. Small discrepancies become larger ones. By year end, the cleanup is significantly more time-consuming than monthly reconciliation would have been. In the worst case, financial statements are materially misstated, tax filings are incorrect, and clients face penalties.