.webp)

.svg)

Common Accounting Mistakes and How to Avoid Them

Blog Summary / Key Takeaways

- Late discovery drives the most expensive accounting errors.

- Most issues fall into the same buckets each month.

- Reconciliations catch balance sheet drift early.

- Flux review catches P&L misclassification fast.

- A review-first close reduces financial reporting mistakes.

- Tools like Xenett help teams standardize review and execution.

What Counts as an “Accounting Mistake” vs. an “Accounting Error”?

Accounting mistakes come from the workflow. Accounting errors show up in the records. You need to fix both, but you fix them in different ways.

Accounting Mistakes

Accounting mistakes happen when the process fails. For example, someone skips a step, or a reviewer does not look at the same accounts each month.

Common operational bookkeeping mistakes include:

- No clear close calendar

- Rushed cut-off work

- Inconsistent review notes

- Decisions made in Slack with no record

- “Looks fine” sign-off with no support

Accounting Errors

Accounting errors live inside the GL. You can point to the line and say, “That is wrong.”

Common accounting errors include:

- Wrong account

- Wrong period

- Wrong amount

- Duplicate entry

- Wrong vendor or customer coding

Why This Distinction Matters

- “Errors” are what you see in the GL.

- “Mistakes” are the system that created them (and will keep creating them until fixed).

In practice, most small business accounting mistakes start as workflow gaps. They turn into month-end accounting errors during reporting.

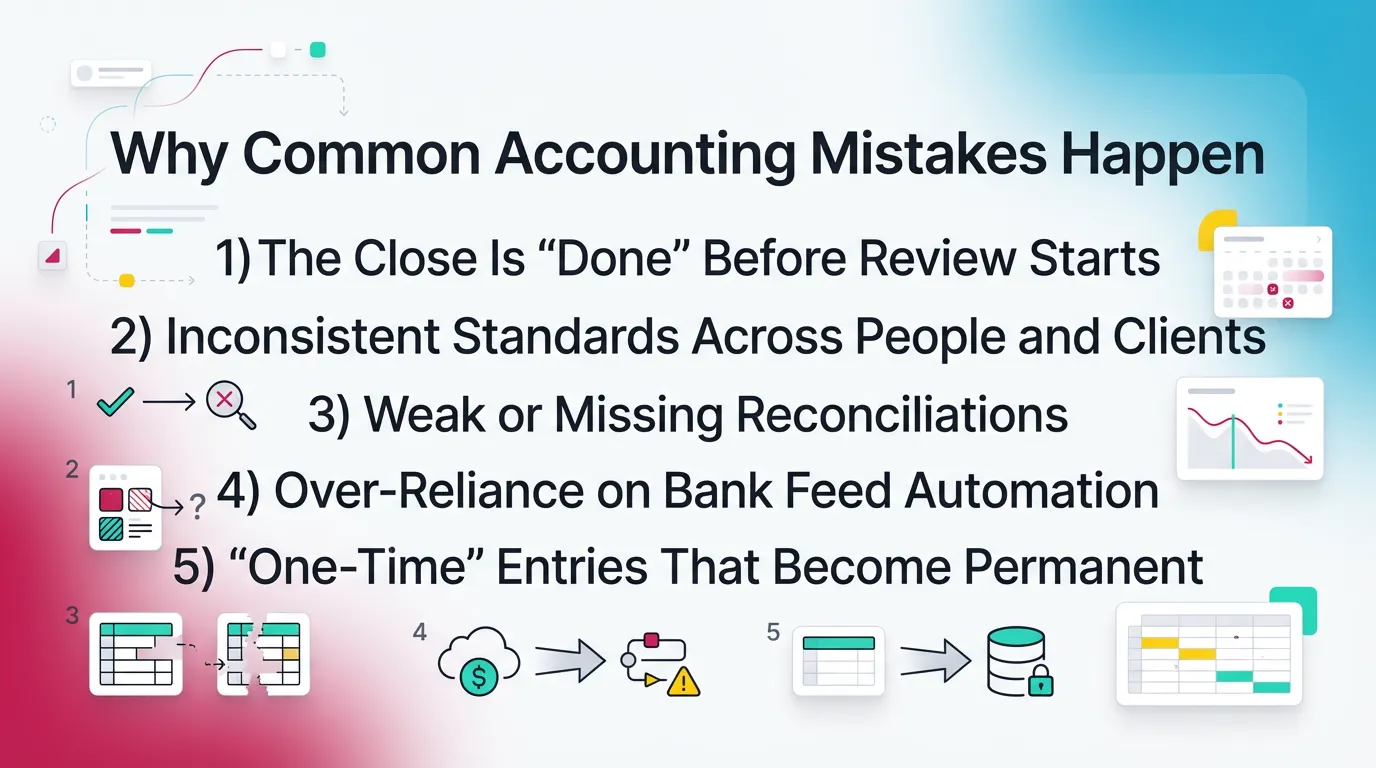

Why Common Accounting Mistakes Happen (Root Causes)

These root causes show up in firms and in-house teams. They also show up in every accounting software stack.

1) The Close Is “Done” Before Review Starts

Teams mark tasks complete before anyone tests reasonableness. Therefore, review turns into cleanup.

A practical example:

A staff accountant “finishes” AP. The reviewer later finds old credits. The team then reopens AP, cash, and expenses.

2) Inconsistent Standards Across People and Clients

Review depends on who looks. One person checks payroll liabilities. Another person does not. That creates uneven risk.

This also causes financial reporting mistakes across entities. Two clients can look “done,” but only one truly is.

3) Weak or Missing Reconciliations

Accounting reconciliation errors do not announce themselves. They build quietly.

When month-end pressure hits, the gap shows up as:

- “Why is cash off?”

- “Why do we have a negative liability?”

- “Why does the credit card not match the statement?”

4) Over-Reliance on Bank Feed Automation

Bank rules speed up coding. However, they can misclassify at scale.

For example:

- A rule posts every “Apple” charge to supplies.

- Half of those charges belong to software or devices.

- Margin and OpEx trends then become noise.

5) “One-Time” Entries That Become Permanent

Teams use “misc expense” or “suspense” to move fast. Then no one comes back.

This creates:

- A growing pile of uncategorized items

- Harder reviews each month

- A recurring set of accounting mistakes examples with no owner

The Most Common Accounting Mistakes (With Real-World Examples + Fixes)

The list below targets the most common causes of rework. It also covers the accounting errors that distort financial statements.

Featured snippet target: Use a numbered list format in the published article.

1) Not Reconciling Balance Sheet Accounts (Accounting Reconciliation Errors)

This is the most common root cause of broken reporting. If the balance sheet does not tie, the P&L also becomes suspect.

Examples

- Bank rec not completed (or completed but unreconciled items aren’t investigated).

- Credit cards don’t tie to statements.

- Payroll liabilities drift.

Impact

- Cash wrong, liabilities wrong, and downstream reporting becomes unreliable.

- Teams spend hours hunting for differences.

- Review becomes reactive instead of planned.

How to prevent

- Standardize reconciliations (who/when/how), require supporting docs, and review exceptions monthly.

- Reconcile cash first. Cash drives trust.

- Age reconciling items. Treat old items as defects.

2) Misclassifying Expenses (Bookkeeping Mistakes That Distort Margin)

Misclassification rarely changes cash. It changes decisions. That makes it dangerous.

Examples

- Repairs coded to CapEx (or vice versa).

- Software subscriptions split inconsistently between COGS/OpEx.

- Owner draws coded as payroll expense.

Impact

- Margin and department profitability become noise.

- Budget vs. actual becomes harder to explain.

- Trend lines stop telling the truth.

How to prevent

- Lock a consistent chart-of-accounts mapping and define “classification rules” for recurring vendors.

- Maintain a “vendor coding dictionary.”

- Require notes for exceptions above a threshold.

Practical experience note:

In multi-client closes, I see this most in “software” and “contract labor.”

Teams code based on the memo line, not the vendor. Fix the rule.

3) Missing Accruals and Prepaids (Month-End Accounting Errors)

Accrual and prepaid misses drive avoidable volatility. They also create the most common “why did profit swing?” questions.

Examples

- Not accruing invoices received after month-end for services already delivered.

- Insurance booked fully in one month instead of prepaid amortization.

- Interest not accrued.

Impact

- P&L swings, misleading trend lines, decision-making based on timing artifacts.

- Forecasting loses accuracy.

- Teams post last-minute true-ups with weak support.

How to prevent

- Accrual checklist + recurring journal entry logic + variance review for key accounts.

- Use a consistent cut-off rule.

- Review “expenses with lag” each month.

4) Duplicate Entries

Duplicate entries often come from good intentions. Someone tries to “make sure it is in.” The system already imported it.

Examples

- Vendor bill entered manually and also imported.

- Bank feed posted and then invoice paid separately without matching.

Impact

- Expenses overstated; AP aging becomes unreliable; cleanup takes hours.

- Teams lose trust in AP and in cash forecasts.

How to prevent

- Enforce “one source of truth” per transaction type and review duplicates via account-level anomaly checks.

- Decide who owns bill entry.

- Train the team to match, not re-enter.

5) Revenue Timing Errors (Especially for Services + Projects)

Revenue timing errors create the loudest questions. Leaders watch revenue first.

Examples

- Deposits recorded as revenue.

- Revenue recognized before delivery milestones.

- Invoices booked in the wrong period.

Impact

- Revenue trends unreliable; deferred revenue incorrect; forecasting breaks.

- Customer profitability becomes misleading.

- Month-end accounting errors show up as late adjustments.

How to prevent

- Clear policy for deposits/deferred revenue + monthly reconciliation of deferred revenue and AR cut-off checks.

- Reconcile deposits to the liability account.

- Test cut-off around month-end dates.

6) Not Reviewing AR/AP Aging for Stale Items

Aging reports are not just collections tools. They are error reports.

Examples

- Old receivables never written off or reserved.

- Vendor credits not applied.

- AP includes bills already paid but not matched.

Impact

- Working capital metrics wrong; cash forecasting suffers.

- Leaders chase “past due” items that are not real.

- The close drags because balances never clear.

How to prevent

- Monthly aging review with explicit actions (collect, dispute, write off, apply credits).

- Add owners and due dates for each action.

- Track “aging clean-up” as part of close.

7) Overusing “Ask My Accountant,” Suspense, or Uncategorized Accounts

These accounts help when used briefly. They harm when used as parking lots.

Examples

- Items parked in suspense with no owner.

- “Cleanup later” becomes “never.”

Impact

- Hidden misclassifications and unresolved recon items.

- Reporting stays unstable.

- Review time grows every month.

How to prevent

- Set thresholds + aging rules for suspense and require monthly clearance.

- For example, no item older than 30 days.

- Require a comment for each remaining balance.

8) Sales Tax / VAT Mis-postings (Compliance Risk)

Tax posting errors create compliance risk. They also create bad liability balances.

Examples

- Tax recorded to revenue or expense accounts.

- Incorrect nexus/jurisdiction mapping.

- Manual adjustments without documentation.

Impact

- Filing issues, penalties, time-consuming corrections.

- Liability accounts stop tying to returns.

- Audits and notices become harder to resolve.

How to prevent

- Separate tax liability accounts + reconciliation between filings and GL + documented adjustments.

- Tie each filing period to the GL balance movement.

- Keep support for every adjustment.

9) Inventory / COGS Mismatch

If inventory exists, you must tie the subledger. Otherwise, gross margin becomes fiction.

Examples

- Purchases expensed instead of inventory.

- Inventory adjustments posted without support.

- COGS not tied to inventory movement.

Impact

- Gross margin meaningless; balance sheet inaccurate.

- Shrink and write-downs hide inside COGS.

- Planning breaks for purchasing teams.

How to prevent

- Tie inventory subledger to GL monthly; investigate unusual COGS % swings.

- Require support for adjustments.

- Review inventory reserve logic each quarter.

10) Financial Reporting Mistakes: Publishing Reports Without a Final Review Pass

This creates the highest reputational cost. People remember revised financials.

Examples

- Sending financials without flux review.

- No sign-off trail on key accounts.

- No documentation for judgment calls.

Impact

- Revisions, loss of trust, repeated rework each month.

- Leaders stop using the numbers.

- The accounting team becomes “the cleanup team.”

How to prevent

- Formal review/approval workflow + documented findings + consistent standards.

- Require a final “ready to issue” sign-off.

- Store review notes where the team can find them.

How Accounting Mistakes Show Up in Financial Statements

You can often spot the error type by the symptom. Use this map before you dig into detail.

P&L Symptoms

P&L symptoms usually point to misclassification or timing. Look for trend breaks first.

- Unexpected margin changes

- Expense spikes/dips

- “Other expense” growing over time

Common causes:

- Bookkeeping mistakes in coding

- Missing accruals or prepaids

- Duplicate entries

Balance Sheet Symptoms

Balance sheet symptoms usually point to reconciliation gaps. Therefore, start with tie-outs.

- Reconciliations not tying

- Negative asset balances (e.g., negative prepaid)

- Liabilities that never clear (payroll, sales tax, credit cards)

Common causes:

- Accounting reconciliation errors

- Stale AR/AP items

- Suspense accounts not cleared

Cash Flow Symptoms

Cash flow symptoms often reveal working capital issues. Profit can look fine while cash drops.

- Profit up, cash down (timing + AR/AP issues)

- Large swings driven by working capital accounts

Common causes:

- AR aging not reviewed

- AP includes duplicates or missing matches

- Revenue timing errors

Month-End Close: Where Accounting Errors Cluster (And Why)

Month-end concentrates activity. That also concentrates risk. The problem is not volume alone. The problem is timing.

The “Late Discovery” Problem

Late discovery creates cascading rework. One fix forces three more.

For example:

- You find a bank recon issue late.

- You fix cash.

- You now must retest AR, AP, and revenue cut-off.

That is why late month end accounting errors cost more than early ones.

Common Month-End Accounting Errors by Stage

Errors cluster by stage because the team focuses on different tasks at different times.

During booking

Booking errors happen fast. They also look “normal” until review.

- Cut-off misses, miscoding, missing accruals

Controls that help:

- Vendor rules for recurring spend

- Clear cut-off timing

- Accrual triggers for known lags

During reconciliation

Reconciliation errors often come from missing support. Or they come from drift that no one owns.

- Unexplained reconciling items, missing statements, unresolved variances

Controls that help:

- Owner per reconciliation

- Required support attached or linked

- Aging rules for reconciling items

During review

Review catches what booking and reconciliation miss. However, review fails when it starts too late.

- Flux anomalies, unsupported balances, inconsistencies across periods/clients

Controls that help:

- Review early, then assign fixes

- Track open items like tasks, not like notes

- Require sign-off and documentation

A Practical Framework To Prevent Common Accounting Mistakes (Without Turning This Into a Checklist-Only Page)

You can reduce accounting mistakes without making close feel heavier. You just need a simple control stack. Then you apply it the same way each month.

The 4-Layer Control Stack (Simple, Repeatable)

- Data hygiene (bank feeds, rules, source documents)

- Reconciliations (bank/CC, AR/AP, key liabilities)

- Account-level review (reasonableness + flux + anomalies)

- Approval + documentation (sign-off + audit trail of decisions)

This stack works because each layer catches different error types.

It also makes ownership clear.

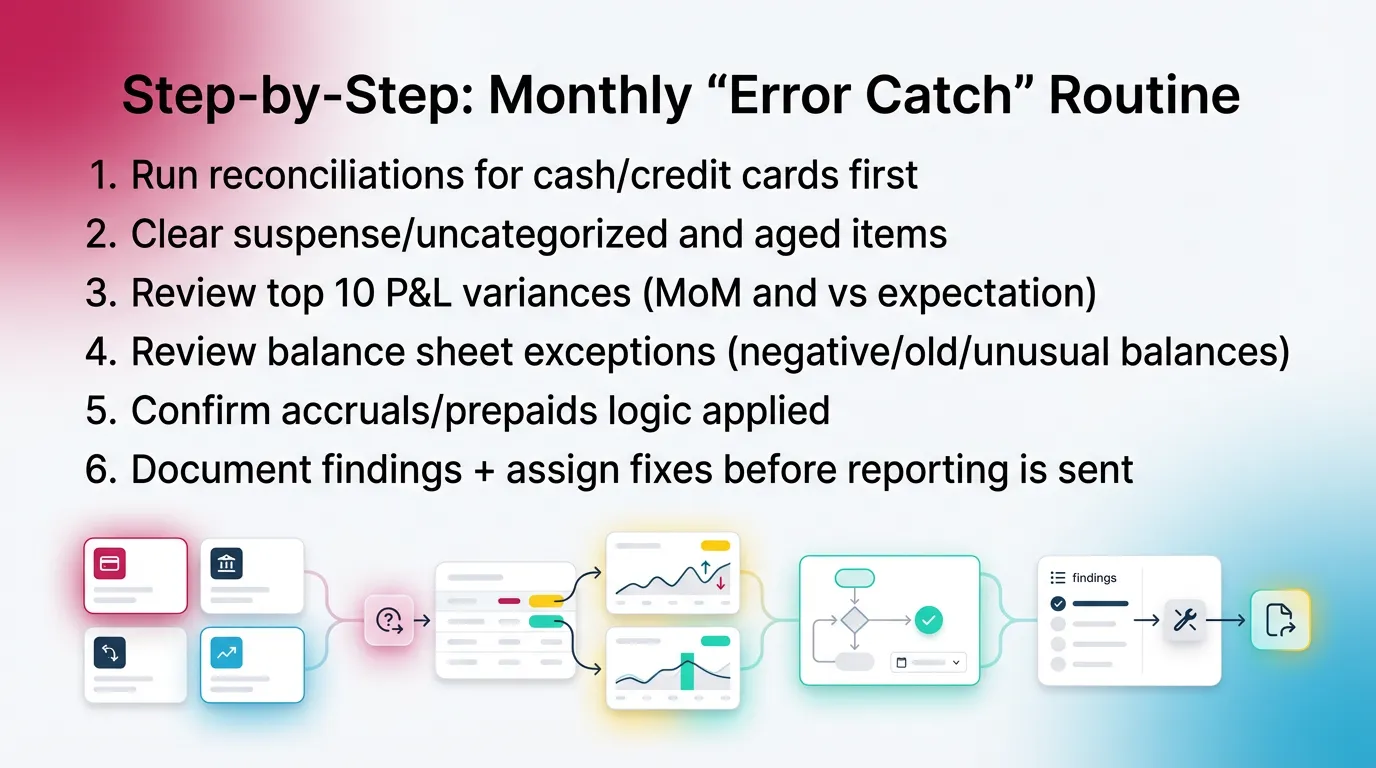

Step-by-Step: Monthly “Error Catch” Routine (60–90 Minutes Per Entity, Scales With Complexity)

This routine catches the most common accounting errors early. It also reduces financial reporting mistakes later.

- Run reconciliations for cash/credit cards first

- Clear suspense/uncategorized and aged items

- Review top 10 P&L variances (MoM and vs expectation)

- Review balance sheet exceptions (negative/old/unusual balances)

- Confirm accruals/prepaids logic applied

- Document findings + assign fixes before reporting is sent

One practical tip:

Set a variance threshold. Use both percent and dollars.

For example, investigate anything over 15% and $2,500.

Adjust by entity size.

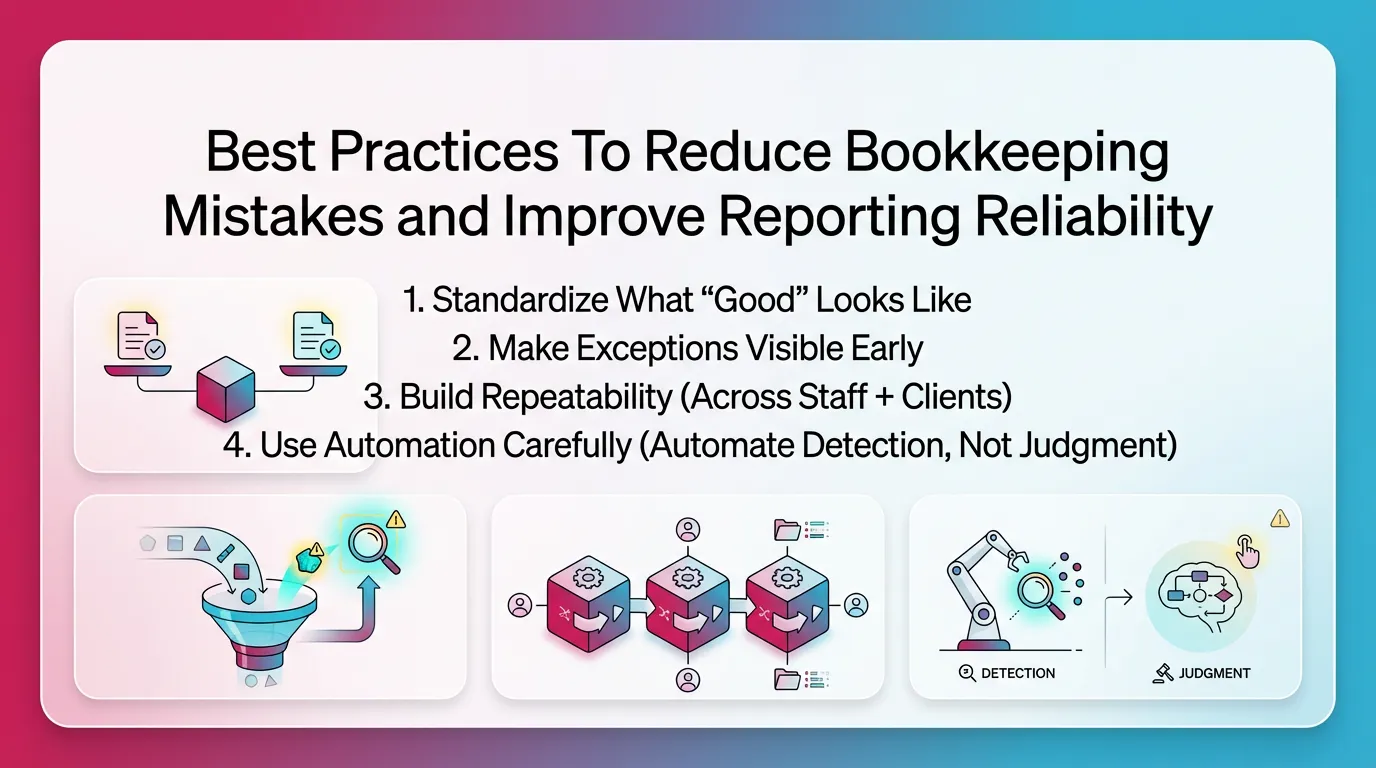

Best Practices To Reduce Bookkeeping Mistakes and Improve Reporting Reliability

These practices help small business accounting mistakes and enterprise errors alike. The difference is volume, not the pattern.

Standardize What “Good” Looks Like

Write down your standards. Keep them short. Use them every month.

- Account-level expectations (what should fluctuate, what should not)

- Thresholds for investigation (variance %, $)

- Required support by account type

For example:

- Payroll liabilities must tie to reports monthly.

- Sales tax payable must tie to filed returns.

- Prepaids must not go negative.

Make Exceptions Visible Early

Surface issues before “final review.” Otherwise, you create late discovery.

- Review should drive the work.

- Booking should support the review.

A helpful habit:

Hold a mid-close review checkpoint.

Review cash, AR, and key accruals before the team books “the rest.”

Build Repeatability (Across Staff + Clients)

Repeatability reduces reliance on memory. It also reduces training time.

- Consistent close calendar

- Consistent review templates by client type

- Clear ownership for each account group

This matters in firms. It also matters in hybrid teams.

Turn “tribal knowledge” into simple rules.

Use Automation Carefully (Automate Detection, Not Judgment)

Automation helps you find anomalies. It does not decide the accounting.

- Automate flags for anomalies and missing steps

- Keep judgment with the accountant

For example:

- Flag duplicate amounts and dates in expense accounts.

- Flag negative asset balances.

- Flag liabilities that never clear.

How Xenett Helps Teams Operationalize Error Prevention During Close (Without Relying on Memory)

Xenett helps teams turn review into a repeatable workflow. It does not replace accounting judgment. It also is not an audit tool and does not provide audit services.

Dedicated Xenett section (required): Position Xenett as a review-first way to apply the best practices above—non-promotional, educational.

Review-First Close: Findings Drive the Work

Xenett helps teams start with account-level review. It surfaces what looks off early. Therefore, the team fixes issues before reporting starts.

- Xenett is built around account-level P&L and balance sheet review, so issues are identified early (before close is “done”).

- Instead of relying on individual reviewer habits, review standards can be made consistent and repeatable.

Close Task and Checklist Management (Structured, Not Ad-Hoc)

Xenett helps connect review findings to execution. The work stops living in scattered notes.

- Close tasks are organized around resolving specific review findings (e.g., “Investigate A/R aging variance,” “Clear unapplied vendor credit”).

- Checklists become tied to account behavior and month-end requirements, reducing missed steps.

This helps reduce bookkeeping mistakes that come from skipped steps.

It also helps reduce month end accounting errors that come from late fixes.

Review and Approval Workflows (Clear Accountability)

Xenett helps teams separate prepared work from approved work. That separation prevents silent failure.

- Supports review sequencing and sign-off so accounts aren’t treated as complete without visibility into what was reviewed and what’s still open.

- Helps teams separate “prepared” from “reviewed/approved,” which is where many month-end accounting errors slip through.

Visibility Into Close Status and Bottlenecks

Xenett helps you see blockers early. That matters most when you run many closes at once.

- Makes it easier to see what’s blocking completion (e.g., missing reconciliation support, unresolved anomalies, pending approvals).

- Useful for multi-client accounting firms managing many closes in parallel.

Accuracy, Audit Trail, and Repeatability (Without Calling It an Audit Tool)

Xenett creates a durable record of what the team reviewed and changed. This supports consistency and clean handoffs.

- Creates a durable record of findings, actions taken, and approvals—useful for internal consistency and client communication.

- Emphasizes repeatable review logic rather than one-off cleanup.

Common Accounting Mistakes: Summary Table (For Fast Scanning)

FAQ: Common Accounting Mistakes

What are some common mistakes in accounting?

Common accounting mistakes include failing to reconcile accounts, misclassifying expenses, missing accruals/prepaids, duplicate entries, revenue timing errors, and publishing financials without a documented review and approval step.

These issues often become expensive when teams find them late in close.

What is the difference between bookkeeping mistakes and accounting errors?

Bookkeeping mistakes are process and data-entry issues (coding, duplicates, missing transactions). Accounting errors include broader record problems that impact financial statements (wrong period, missing accruals, incorrect balances).

In practice, bookkeeping mistakes often cause accounting errors downstream.

What are the most common month-end accounting errors?

The most common month-end accounting errors are missed reconciliations, incomplete accruals, uncleared suspense/uncategorized items, and last-minute adjustments made without documentation or review.

You can prevent most of them with early reconciliations plus flux review.

How do accounting mistakes affect financial reporting?

Accounting mistakes can overstate or understate profit, misstate assets and liabilities, distort cash flow, and reduce confidence in monthly reporting—often leading to rework and delayed close.

They also reduce trust in trends, budgets, and forecasts.

What are the 6 types of errors in accounting (with examples)?

A commonly cited set includes: errors of omission (missing entry), commission (wrong account), principle (violates accounting treatment), original entry (wrong amount posted), transposition (digits swapped), and compensating errors (two errors offset).

Example: transposing 1,530 as 1,350.

What’s the fastest way to catch accounting reconciliation errors?

Reconcile cash and credit cards first, then review reconciling items by age and size, and require documentation for unresolved differences. Pair reconciliations with an account-level flux/anomaly review so you catch issues that “technically reconcile” but still don’t make sense.

How can small businesses reduce accounting mistakes without adding headcount?

The most effective approach is standardizing monthly routines (reconciliations + variance review), documenting rules for common transactions, and using systems that make review findings visible early so fixes happen before reporting is finalized.

This approach reduces small business accounting mistakes without adding more people.

Conclusion

Common accounting mistakes repeat because the workflow allows them to repeat. Fix the workflow and you reduce the errors. Start with reconciliations, then run account-level review, then require sign-off with documentation.

If you want fewer month end accounting errors next month, pick one change and make it standard. For example, reconcile cash first and age reconciling items. Then add a top-10 flux review.

If you manage multiple entities or clients, consider moving to a review-first close workflow in Xenett. Use it to standardize review, track findings as work, and keep approvals visible before you send financials.