.svg)

Month-End Close Best Practices: Procedures & Standards

Blog Summary / Key Takeaways

- Month-end close best practices are not about working faster they are about eliminating late discovery, which is the root cause of rework, delays, and inconsistent financials that you end up explaining twice.

- The close runs most predictably when you follow the same 7-step sequence every period from pre-close prep through a post-close retrospective with defined outputs and evidence requirements at every step.

- Review must happen earlier, by account group as work completes, not after reports are drafted shifting review timing reduces rework faster than any other single change.

- Setting flux thresholds, reconciling-item aging rules, and JE support requirements in writing is what makes review consistent across staff without written standards, quality depends on who reviews that month.

- Xenett supports a review-first close by standardizing account-level P&L and balance sheet checks, surfacing anomalies and exceptions early, and keeping resolution work visible until accounts clear so close quality holds up across multiple clients, entities, and reviewers.

Month-End Close Best Practices: Procedures & Standards

Late review creates rework. Rework creates delays. And delays create inconsistent financials that you end up explaining twice.

Month end close best practices work when you treat the close like a controlled process, not a sprint at the end of the month. You need repeatable procedures, clear standards, and evidence-based review especially if you manage multiple entities or multiple clients.

Quick Answer

Month end close best practices are repeatable procedures, controls, and review standards that help you produce accurate monthly financials on a predictable timeline. They reduce errors by enforcing cutoffs, completing reconciliations with aging rules, and requiring documented review sign-offs. They reduce rework by moving account-level review earlier in the close.

The Steps and Best Practices

The close is fastest when you run the same steps every month and hold the same "done" standards each time. You do not win by moving tasks faster. You win by reducing late discoveries.

Use this section as your reference block. Then use the rest of the guide to implement standards, ownership, and controls that hold up under pressure.

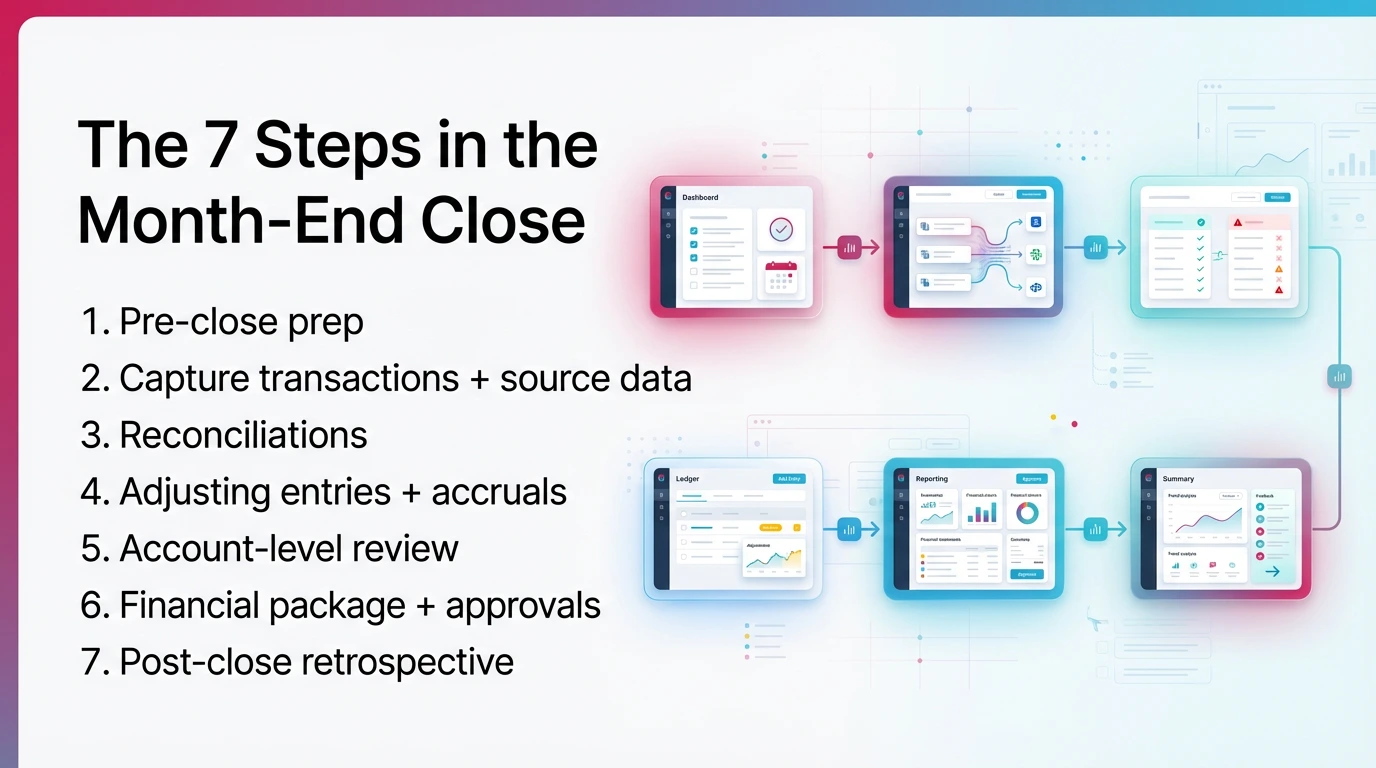

The 7 Steps in the Month-End Close

- Pre-close prep: publish calendar, cutoffs, and open items list.

- Capture transactions + source data: confirm AP/AR, payroll, bank feeds, billing inputs.

- Reconciliations: complete key balance sheet recs and assign reconciling items.

- Adjusting entries + accruals: post supported accruals, deferrals, and recurring entries.

- Account-level review: run flux checks, tie-outs, and reasonableness tests.

- Financial package + approvals: finalize reporting pack and obtain sign-offs.

- Post-close retrospective: log repeat issues and change next month's standards.

Top 10 Best Practices for Month End Closing

Top 10 Best Practices for Month End Closing

- Publish cutoffs in writing and enforce them

- Start review earlier by account group, not after reports run

- Reconcile high-risk accounts weekly, not monthly

- Use reconciling-item aging rules with owners and deadlines

- Tie subledgers to the GL every close (AR/AP/payroll)

- Require support attachments for material journal entries

- Use consistent flux thresholds by account type

- Separate operational entries from true-up entries

- Lock periods fast and define reopen rules

- Run a short retro that produces process changes

What Are Month-End Close Best Practices?

Month-end close best practices are the operating rules that make your close repeatable. They define how you collect inputs, reconcile balances, post adjustments, and review accounts so you can lock the period with confidence.

Month-end close best practices are defined as repeatable procedures, controls, and review standards that produce accurate financials on a predictable timeline, with documented support and clear approvals.

When "best practices" work, you see the same outcomes month after month. You do not rely on one senior reviewer, a late-night cleanup journal entry, or "we'll fix it next month."

What "Good" Looks Like (Operational Outcomes)

A healthy close looks boring in the best way:

- You close on a predictable day, not a moving target.

- You post fewer post-close adjustments and reversals.

- You review both balance sheet and P&L consistently.

- You keep a clean evidence trail for key balances.

- You can hand off review across staff without changing quality.

Symptoms Your Close Needs Process Improvements

If you see these patterns, your close lacks standards, not effort:

- Tasks show "done," then review restarts the work.

- Reconciling items sit for months with no owner.

- Flux explanations happen at the end, under time pressure.

- Review comments change based on who reviews.

- One big cleanup JE "makes it work" at the finish.

Those symptoms usually share one root cause. You treat review as a final step. However, review is the control system of the close. When you move it earlier, rework drops fast.

Month-End Close Procedures: The Standard 7-Step Process (With Inputs + Outputs)

Your close runs smoother when you standardize the procedure and define the outputs for each step. You do not need a complicated workflow. You need clear inputs, clear outputs, and evidence requirements.

Before the step-by-step detail, use this mini table as your extraction-ready reference.

Step → Output → Evidence Required

Step 1: Pre-Close Prep

You set the close up for success by controlling timing and dependencies before day one. If you skip prep, you spend the close negotiating cutoffs and waiting for inputs.

Inputs: prior month open items, known recurring entries, upcoming deadlines.

Work: publish calendar, send cutoff reminders, confirm system feeds.

Review checks: confirm owners and due dates for high-risk accounts.

Output: close calendar, cutoff reminders, open items list.

What to standardize:

- Close calendar by day (Day -2 through Day +X).

- Cutoff policy in plain language (what goes in this month vs next).

- Intake rules for late bills, late payroll, and late revenue items.

A practical example: you can avoid a day of rework by setting a payroll cutoff. You accrue late payroll with support instead of waiting and rerunning every report.

Step 2: Capture Transactions + Source Data

You close what you captured. If your source data arrives late or incomplete, review turns into cleanup.

Outputs: complete subledger inputs, bank feed status, missing documentation list.

What to capture and confirm:

- AP completeness (bills entered, approvals complete, cutoff applied).

- AR completeness (invoices issued, credits applied, collections posted).

- Payroll posted or accrued (wages, taxes, benefits).

- Bank and card feeds updated (or statements imported).

- Billing and revenue inputs finalized (especially for service firms).

If you run multiple entities or clients, track this as a simple intake log. You want one place that says "received," "missing," and "blocked."

Step 3: Reconciliations

Reconciliations prove balance sheet integrity. If you only reconcile at month-end, you stack risk and create a review bottleneck.

Outputs: reconciliations completed, reconciling items aged and assigned with owners.

Run these first:

- Bank and credit cards (cash is your control account for reality).

- AR and AP control accounts tied to aging.

- Payroll liabilities tied to payroll reports and payments.

- Clearing and suspense accounts that should net to zero.

- Intercompany balances for multi-entity groups.

Use a real aging rule. For example:

- 0–30 days: explain and monitor

- 31–60 days: assign owner and action date

- 61–90 days: escalate to controller/partner

- 90+ days: require written resolution plan or write-off decision

For deeper reconciliation workflow detail, see Xenett's guide on account reconciliation.

Step 4: Adjusting Entries + Accruals

Adjusting entries should not feel like "cleanup." They should follow templates, carry support, and align to a reversal policy.

Outputs: JE support pack, accrual schedule, reversal policy alignment.

What to post here:

- Recurring entries (depreciation, amortization, prepaid amortization).

- Accruals with support (payroll, contractor costs, interest, utilities).

- Deferrals (prepaid expenses, deferred revenue where applicable).

- True-ups separated from operational entries.

A simple rule that reduces review time: do not post one large adjustment JE that touches 20 accounts. Post smaller entries with clear memos and attachments.

If your accrual accounting process is inconsistent, this guide helps you tighten the mechanics.

Step 5: Account-Level Review

Account-level review is where you prevent late surprises. You review accounts first, then you trust the reports.

Outputs: flux notes, exceptions log, cleared questions list.

Review in this order:

- Balance sheet integrity (recs, clearing, negatives, stale items).

- P&L reasonableness (flux, miscodes, missing accruals).

- Tie-outs (subledgers to GL, key schedules to balances).

Keep an exceptions log. Make it visible. Every exception needs one of three outcomes:

- resolved and supported

- formally deferred with rationale

- escalated for decision

Step 6: Financial Package + Internal Approval

The financial package is the output of a controlled close. It should not be the starting point for review.

Outputs: final financial package, variance commentary, sign-offs, client-ready version (for firms).

Minimum package components:

- Balance sheet and P&L.

- Cash flow (if applicable).

- Variance commentary tied to flux thresholds.

- Exceptions log summary (what was resolved vs deferred).

- Approval record (who approved what and when).

Once approvals happen, lock the period. Then enforce a change control rule for anything that reopens it.

Step 7: Post-Close Retrospective + Improvement Loop

The retro is how your close gets faster without losing accuracy. You convert pain into standards.

Outputs: top 5 repeat issues, control gaps, action owners, next month changes.

Keep the retro short:

- Top 5 rework drivers (not top 20 complaints).

- One control you add next month.

- One standard you clarify next month.

- One metric you watch next month.

Then update your checklist. If the retro does not change the next close, it is just a meeting.

Month-End Close Standards (What Must Be True Before You Call It "Closed")

Month end close standards define "done." They stop debates and reduce review back-and-forth. Without standards, you rely on judgment calls under time pressure.

Think of standards in four buckets: evidence, review, posting, and lock/change control. When you document these, you can onboard staff faster and reduce reviewer bottlenecks.

Evidence Standards (Minimum Support by Balance Category)

Set minimum evidence by category. Do not leave it to personal preference.

A practical baseline:

- Cash (banks/cards): reconciliation report + statement + aging of reconciling items

- AR: aging report + tie-out to GL + explanation of any delta

- AP: aging report + tie-out to GL + cutoff confirmation

- Payroll liabilities: liability detail + payment support + accrual calc

- Accruals/deferrals: schedule + assumptions + reversal note (if applicable)

- Fixed assets: rollforward + support for additions/disposals

- Clearing/suspense: detail + plan to clear remaining items

- Intercompany: entity-to-entity tie-out + settlement plan

Retention rule: store evidence in a consistent location, linked by account and period. You want a second reviewer to reperform quickly.

Review Standards (Flux Thresholds, Reasonableness, Tie-Outs)

Review standards reduce subjective review. They also reduce the "review style" problem across seniors.

Use a simple 3-part standard:

- Account behavior: does the account behave as expected? Use flux thresholds.

- Tie-outs: does the subledger or schedule tie to the GL?

- Reasonableness: does the number make sense given volume or activity?

Set flux thresholds by account type. For example:

- Revenue: >10% and >$X

- Payroll: >5% and >$X

- Discretionary spend: >15% and >$X

- Balance sheet: any negative where it should not be negative

Write the thresholds down. Then enforce them.

Posting Standards (JE Format, Approvals, Attachments)

Posting standards reduce review time more than "more review."

Minimum JE standards:

- Clear memo that explains the why, not just the what

- Consistent naming for recurring entries

- Required attachments for material entries

- Approval tiers (for example, >$10k requires controller approval)

You also want a policy for late entries. Decide what gets accrued vs pushed to next month.

Lock & Change Control Standards (Period Lock, Reopen Rules, Audit Trail)

Locking the period is a control. It prevents silent changes that destroy trust.

Define:

- who locks the period

- when you lock (immediately after approvals)

- what triggers a reopen (material error, client-requested change)

- who approves reopen (controller/partner)

- how you document the change (JE, memo, revised package, timestamp)

If you do not define this, you will reopen periods casually. Then your "final" numbers stop being final.

Close Ownership and Deliverables (Procedure-Level Clarity)

Close ownership makes the procedure executable. If ownership is vague, your close slows down because people wait, not because work is hard.

Use a simple RACI. Keep it consistent across clients and entities. Then define what "done" produces so review does not chase missing workpapers.

Roles / RACI (Who Prepares vs Reviews vs Approves)

Include non-accounting dependencies too:

- AP owner for invoice cutoff

- AR/billing owner for invoicing cutoff

- Payroll owner for payroll timing

- Ops for inventory or project inputs

Close Deliverables (What "Done" Produces)

Your close should produce the same deliverables every month:

- Reconciliation pack (key balance sheet accounts)

- JE support pack (material entries with attachments)

- Variance commentary (based on thresholds)

- Exceptions log (resolved vs deferred)

- Final financial package (internal and client-ready, if needed)

- Period lock confirmation (and audit trail)

If any deliverable is missing, you are not closed. You are just out of time.

Why Month-End Closes Run Late (Root Causes Mapped to the Process)

Month-end closes run late for predictable reasons. You can fix them when you tie each delay to a step and a standard.

Most teams blame "too much work." However, the real driver is late discovery. You find issues when the clock is tight, so every fix creates rework.

Late Source Data (AP/AR/Payroll/Banks)

Late source data breaks Step 2 and creates chaos in Steps 4–6. You cannot review what you do not have.

Fix it with:

- enforced cutoffs (Step 1 standard)

- an intake log (Step 2 output)

- accrual rules for late items (Step 4 standard)

For example, if payroll arrives late every month, stop waiting. Accrue with a template and reverse next month when payroll posts.

Reconciliations Done but Not Investigated

A "completed" reconciliation with 90-day items is not complete. It is a delayed problem.

Fix it with:

- reconciling-item aging SLAs (Step 3 standard)

- owner assignment for each aged item (Step 3 output)

- escalation rules (controller/partner review)

Reviewer Bottlenecks (Inconsistent Standards)

When review standards vary, reviewers ask different questions. The team loops through multiple revisions.

Fix it with:

- documented review thresholds (Step 5 standard)

- an exceptions log (Step 5 output)

- staged review (review high-risk accounts early, not all at the end)

Manual Journal Entry Risk (Big Cleanup JEs)

Large unsupported JEs create late review time and increase post-close adjustments.

Fix it with:

- JE templates and required attachments (Step 4 standard)

- approval tiers (Step 4 standard)

- smaller entries with clear memos (Step 4 practice)

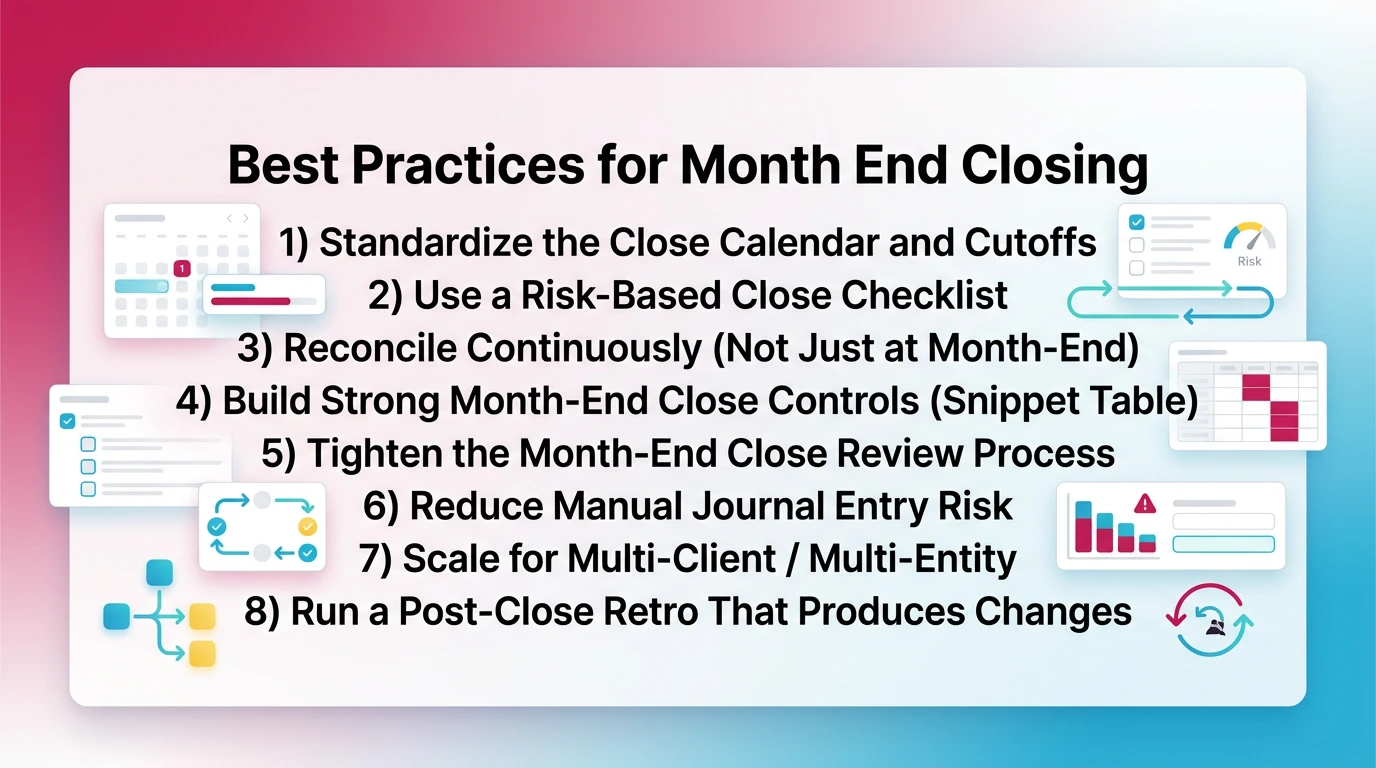

Best Practices for Month End Closing (Review-First Improvements)

You improve your month-end close by changing review timing and standardizing evidence. These are the levers that reduce rework without lowering quality.

The best practices below do not repeat the 7-step process. They make the process run predictably.

1) Standardize the Close Calendar and Cutoffs

A calendar and cutoff policy prevent negotiation during the close. They also protect your review window.

Use a simple cutoff example:

- Day -1: stop entering operational AP for the month at 5pm

- Day 0: accrue late AP items received after cutoff using a standard template

- Day +1: no new postings without approval and documented reason

This aligns with the standard month-end close process.

2) Use a Risk-Based Close Checklist

A checklist should reflect risk, not just tasks. You want checks that prevent known errors and produce evidence.

Use a scannable table:

3) Reconcile Continuously (Not Just at Month-End)

Continuous reconciliation keeps problems small. It also spreads work across the month.

Use a cadence:

- Weekly: bank/cards, clearing/suspense.

- Bi-weekly: payroll liabilities (if payroll is frequent).

- Mid-month: AR/AP tie-outs.

- Month-end: full pack, final aging, escalation.

Apply aging SLAs:

- 0–30 days: explain

- 31–60 days: fix date set

- 61–90 days: escalate

- 90+ days: decision required

4) Build Strong Month-End Close Controls

Controls prevent issues, detect issues early, and force resolution. You need all three.

A control only works if it produces evidence. If it leaves no trail, it does not protect you under review or client questions.

5) Tighten the Month-End Close Review Process

Review needs consistency. You get that from standards, not from more senior time.

Do this:

- Review balance sheet accounts first.

- Stage review by account group as work completes.

- Enforce sign-offs with evidence links.

- Keep an exceptions log to prevent scattered comments.

Reference your review standards section. Do not reinvent review every month.

6) Reduce Manual Journal Entry Risk

Manual JEs are not bad. Uncontrolled manual JEs are.

Reduce risk with:

- templates for common entries

- required attachments for material items

- clear memos that explain assumptions

- separation of operational entries vs true-ups

Avoid a single "cleanup" JE at the end. It hides problems and increases review time.

7) Scale for Multi-Client / Multi-Entity

Scale breaks when every client has custom review logic. Standardization is what makes review transferable.

Standardize:

- account groupings for review (same categories across clients)

- review depth tiers (simple, standard, complex)

- intercompany process timing (tie-outs before consolidation)

- escalation paths (who decides materiality and deferrals)

8) Run a Post-Close Retro That Produces Changes

A retro should change next month's close.

Require these outputs:

- 1–3 standard changes (cutoffs, evidence, review thresholds).

- 1 control addition (preventive/detective/corrective).

- 1 metric you will track next month.

If the retro does not produce changes, it becomes noise.

Month-End Close Efficiency: Metrics and Targets

Month end close efficiency improves when you measure a small set of metrics and act on them. You do not need a dashboard with 40 KPIs. You need a scorecard that explains delays.

Use metrics that map to root causes. Then set targets as ranges. Focus on consistency, not heroics.

Core Metrics to Track

Track these every month:

- Close days: calendar days from period end to lock

- Post-close adjustments: count and dollar value

- Recs completed by Day X: percent complete by a set day

- Average age of reconciling items: especially 60+ and 90+

- Review cycle time: time accounts wait for review

- JE volume and late JEs: how many entries post after review starts

A simple interpretation:

- High post-close adjustments = late discovery

- Old reconciling items = weak reconciliation discipline

- Long review cycle time = bottleneck or unclear standards

- Many late JEs = cutoffs and intake rules not enforced

Starter Targets

Targets vary by complexity. Use these as starting ranges, not promises:

- Close days: 3–8 days depending on entity complexity

- Post-close adjustments: trending down month over month

- Recs completed: 80–90% by Day +2 for key accounts

- Reconciling items: very few items older than 60 days

- Review queue: no account group waiting more than 24–48 hours

If you hit targets only when one senior works late, your system still fails. Your process must perform without heroics.

How to Improve Month-End Close in 30–60–90 Days (Practical Change Plan)

You improve your close by stabilizing first, then standardizing, then automating repeated checks. This keeps the change manageable and reduces disruption.

Each phase should produce three things: one standard created, one control added, and one metric tracked.

30 Days: Stabilize (Make Work Visible)

Direct answer: In the first 30 days, you create a calendar, enforce cutoffs, and define what "done" means. You reduce chaos before you try to optimize.

Do this:

- Publish a close calendar and cutoff policy.

- Create a top-10 risk checklist with owners and due dates.

- Define "done = supported + reviewed."

- Track one metric: post-close adjustments.

Deliverables by Day 30:

- a written cutoff policy

- a checklist with evidence fields

- a basic exceptions log template

60 Days: Standardize (Reduce Reviewer Dependence)

Direct answer: In days 31–60, you standardize review thresholds, reconciliation aging, and JE support rules. You make review consistent across reviewers.

Do this:

- Set flux thresholds by account type.

- Enforce reconciling-item aging SLAs and escalation.

- Create JE templates and approval tiers.

- Track one metric: recs completed by Day X.

Deliverables by Day 60:

- review standards documented

- recon aging rules enforced

- JE policy in place

90 Days: Tighten Controls (Lock + Retro Discipline)

Direct answer: In days 61–90, you implement lock and change control discipline and turn retros into process changes. You reduce repeat issues.

Do this:

- Define period lock and reopen rules.

- Require a retro output: standards change + control + metric shift.

- Start automating repeated checks where possible.

- Track one metric: review cycle time.

If you want month-end close automation ideas that fit accounting reality, also explore how to streamline month-end close.

Month-End Close Best Practices Checklist (On-Page)

This checklist gives you a clean minimum standard you can run every month. It mirrors the 7-step process and forces evidence and review discipline.

Use it as a baseline. Then customize by risk tier (simple vs complex clients/entities).

Pre-Close (Before Day 0)

- Close calendar published with owners and due dates

- Cutoff policy confirmed (AP, AR, payroll, billing, banks)

- Open items list carried forward and assigned

- Recurring entries scheduled and reviewed

- Source system dependencies confirmed (feeds, integrations)

During Close (Day 0 to Day +X)

- Bank and card reconciliations completed with aging

- AR control ties to aging (delta explained if any)

- AP control ties to aging (delta explained if any)

- Payroll liabilities reconciled (payments and accruals supported)

- Clearing/suspense accounts cleared or explained with plan

- Accruals posted using templates with support attached

Review (Account-Level)

- Flux checks run using documented thresholds

- Tie-outs completed (subledger/schedules to GL)

- Exceptions log updated and cleared or deferred with rationale

- Reviewer sign-off recorded with evidence links

Lock and Retro

- Financial package finalized with variance commentary

- Approval captured (who approved, when)

- Period locked and lock evidence stored

- Retro completed with actions, owners, and next month changes

How Xenett Can Help (When You Need More Review Discipline)

You do not need software to run a close. You need software when manual review stops scaling. That usually happens when you manage multiple clients, multiple entities, or multiple reviewers.

When a Checklist Isn't Enough (Signals You've Outgrown Manual Review)

Direct answer: You have outgrown manual review when issues repeat, review outcomes vary by reviewer, and late surprises drive post-close changes. A checklist cannot enforce standards or catch anomalies early across many accounts.

Common signals:

- You manage many clients or entities and cannot see close status clearly.

- Reviewer comments change based on who reviews that month.

- Reconciling items repeat and age without resolution.

- Flux surprises show up late, after tasks are marked "done."

- You see unsupported journal entries that expand review time.

- You reopen closed periods too often.

What Xenett Reinforces (Review-First, Not Workflow-First)

Direct answer: Xenett helps you run a review-first close by standardizing account-level review across the P&L and balance sheet. It surfaces anomalies, flux, missing entries, and reconciliation gaps early, then helps you organize the work to resolve those findings before you lock.

What that looks like in practice:

- You run consistent account-level checks across clients/entities.

- You see exceptions early, not on the last day.

- You attach evidence and keep review sign-offs consistent.

- You track close status and bottlenecks without chasing updates.

Xenett is AI-assisted, not AI-led. It supports review rule setup and interpretation while you keep accounting judgment.

If you want to reduce manual checks and rework, explore month-end close automation and how to streamline month-end close.

Start a 14-day free trial: Try Xenett free

Commercial Investigation: Fit, Dealbreakers, and Switching Guidance

Direct answer: Xenett fits best when review inconsistency and late discovery cost you time each month. It is not a fit if you only want a basic task list or if you do not plan to standardize review rules.

Pros (when you need more discipline)

- Earlier detection of anomalies and missing items

- More consistent review outcomes across reviewers

- Better visibility across many closes at once

- Fewer late-stage review loops

Cons (real tradeoffs)

- You still need to define standards and enforce them

- You must adopt a review-first routine, not "checklist only"

- Setup takes focused time, especially for multi-client environments

Who should use it

- Firms running recurring closes across 10–500+ clients

- Multi-entity teams with intercompany and consolidation timing risk

- Teams with reviewer bottlenecks and inconsistent review quality

Who should not use it

- Teams that do not want to document standards

- Single-entity teams with very low transaction volume

- Anyone looking for AI to replace reviewer judgment

Dealbreakers to check before you switch

- You cannot enforce cutoffs internally

- You do not have clear account ownership

- You do not retain evidence consistently

Pricing clarity

Xenett pricing depends on scale and usage. Check Xenett directly for current pricing and packaging.

Switching guidance

Start with one close cycle and one tier of accounts. Move your highest-risk balance sheet accounts first (cash, AR/AP controls, payroll liabilities, clearing). Then add P&L review rules and flux thresholds.

FAQ: Month-End Close Best Practices

What are month end close best practices?

Month end close best practices are repeatable procedures, controls, and review standards that make monthly financials accurate and predictable. They reduce rework by shifting account-level review earlier, enforcing cutoffs, and requiring consistent evidence for key balances. They also standardize reconciliations, approvals, and period lock rules.

What are the steps in the month-end close process?

Most teams follow seven steps: pre-close prep, capture transactions and source data, complete reconciliations, post adjusting entries and accruals, perform account-level review, finalize the financial package with approvals, and run a post-close retrospective. The key is defining outputs and evidence requirements at every step.

What are month end close standards?

Month end close standards define what must be true before you lock a period. They include required reconciliations with aging rules, support attached to material journal entries, documented flux explanations above thresholds, consistent review sign-offs, and clear lock and reopen rules that preserve audit trail discipline.

How do you improve month end close efficiency without losing accuracy?

You improve month end close efficiency by standardizing cutoffs, reconciling high-risk accounts throughout the month, and enforcing consistent review rules. Accuracy increases speed because you detect issues earlier. That reduces late cleanup, post-close adjustments, and repeated review cycles during the final days of close.

What causes month-end close delays most often?

Late discovery during review causes most month-end close delays. Issues surface after tasks are marked complete, which forces rework and reposting. Common drivers include late source data (banks, payroll, AP/AR), reconciliations not investigated, inconsistent review standards, and large unsupported journal entries posted near the deadline.

What metrics should we track for month end close efficiency?

Track close days, number and value of post-close adjustments, reconciliation completion by day, average age of reconciling items, review cycle time, and journal entry volume with late entries. These metrics show whether delays come from data timing, reconciliation discipline, or reviewer throughput and standards.

How detailed should month-end close documentation be?

Documentation should let a second reviewer validate the conclusion without starting over. That usually means the reconciliation, support for reconciling items, and attachments for material journal entries. Organize it consistently by account and period. Include clear memos, timestamps, and sign-offs so questions do not restart work.

Conclusion

Month end close best practices only work when you protect review integrity. You cannot spreadsheet your way out of late discovery. You need standards that hold up when things get busy.

If you implement only three changes next close, make them these:

- Move account-level review earlier, by account group.

- Define "done" as supported and reviewed, not just posted.

- Track a small scorecard and run a retro that changes next month.

Ready to close faster?

Try Xenett free →